09.01.16

Driven by significant economic growth during the past 15 years, China has surpassed North America and Western Europe to become the largest global consumer and producer of methanol (China now consumes 54 percent of global methanol demand), according to new analysis from IHS Markit .

“The global methanol industry has undergone dramatic changes in the past 15 years, with China becoming the dominant player in the global market,” said Mike Nash, global director of syngas chemicals at IHS Markit. “The Chinese market dominance for methanol and its derivatives, such as for direct gasoline blending and more recently MTO (methanol-to-olefins, which refers to the production of olefins from merchant methanol), is driving a significant shift in market dynamics and adding complexity for both methanol producers and consumers. These factors have resulted in new trade flows, pricing and economic dynamics that did not exist previously.”

According to IHS Markit, which will welcome methanol producers and other industry professionals to its 34th Annual World Methanol Conference in Budapest, Hungary, 30 Sept. – 1 Oct. 2016, in 2000, China represented just 12 percent of global methanol demand, while North America and Western Europe represented 33 percent and 22 percent, respectively. By 2015, Chinese methanol consumption had grown to 54 percent of global demand while North American demand had fallen to 11 percent and Western Europe to 10 percent.

Chinese demand, Nash said, has grown significantly in traditional methanol derivatives, such as formaldehyde and acetic acid, but also in new end-uses, such as light olefins production, as well as expanded demand into energy applications, such as DME (dimethyl ether) and direct gasoline blending.

DME is primarily used as an aerosol propellant in the West, which represents a relatively small market overall. However, DME is also used in fuel applications—where it is mainly blended into liquefied petroleum gas (LPG). This application is widely used by Chinese consumers for home cooking and heating, which has helped drive methanol consumption into DME from virtually nothing in 2000, to the fourth largest methanol derivative in 2015, IHS Markit said.

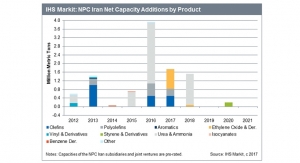

China’s direct blending of methanol into the country’s gasoline pool has driven an average annual growth rate for this application of 25 percent from 2000 to 2015, making gasoline blending the third-largest methanol demand segment. A newer and rapidly growing demand segment for methanol (exclusively in China) is in the production of light olefins using methanol-to-olefins (MTO) technologies. In just four years, this end-use has driven staggering growth in methanol consumption and made MTO the sixth largest end-use for methanol. During the next few years, IHS Markit expects MTO to become the second largest end-use for methanol.

Feedstock costs for methanol comprise as much as 90 percent of the total cash-cost and, as such, access to low-cost feedstocks is key to methanol economics. The primary feedstock for methanol has been natural gas, representing as much as 85 percent of installed global capacity. Regions with access to low-cost natural gas have seen a surge in methanol capacity additions, including the Middle East, Africa and South America. With the growth in Chinese methanol demand and the country’s rich coal reserves, the industry has seen a sharp rise in coal-based methanol production.

Uncompetitive feedstock economics led to capacity rationalizations in North America and Europe in the early 2000s, with North American methanol capacity all but extinguished by 2008. However, recent exploitation of unconventional natural gas supplies in North America has allowed this region to regain its position as a methanol production powerhouse.

The sharp rise in North American production capacities and the cost position of these units has led to an increase in exports from the Americas that now add supply to both the European and Northeast Asian methanol markets. The expected growth in North American capacities will turn the region from a net importer to a net exporter by early 2019, IHS Markit said.

Supply and demand pressures have always driven methanol pricing, but now that methanol has significant volumes of derivatives that compete as alternatives to crude-oil derived products, the picture becomes significantly more complicated, since affordability of some methanol derivatives becomes dependent on crude oil price fluctuations, Nash said.

“Due to this linkage with crude oil markets, to assess the future direction of methanol demand, you have to assess not only the light olefins markets, but also the global fuel markets,” Nash said. ”With the drop in oil prices, methanol demand for these derivatives has been under pressure, with most consumers able to afford a much lower methanol price than in the past. This has been particularly the case for DME.”

The IHS Markit report said the methanol industry will face more moderate demand growth rates as direct-gasoline blending has matured and the feverish pace of MTO projects moderates. Overall demand during the next five years will grow at an average annual rate of almost 7 percent, with MTO becoming the second-largest methanol derivative. IHS Markit expects natural gas prices to remain below $5 U.S. per MMBtu in the next five years, and oil prices to rebound from the currently low level, the growing spread between these two commodities should therefore support methanol demand going forward.

To view the current agenda for the 34th Annual IHS World Methanol Conference, and to register for the event or training workshop, visit https://www.ihs.com/events/annual-wmc/register.html.

“The global methanol industry has undergone dramatic changes in the past 15 years, with China becoming the dominant player in the global market,” said Mike Nash, global director of syngas chemicals at IHS Markit. “The Chinese market dominance for methanol and its derivatives, such as for direct gasoline blending and more recently MTO (methanol-to-olefins, which refers to the production of olefins from merchant methanol), is driving a significant shift in market dynamics and adding complexity for both methanol producers and consumers. These factors have resulted in new trade flows, pricing and economic dynamics that did not exist previously.”

According to IHS Markit, which will welcome methanol producers and other industry professionals to its 34th Annual World Methanol Conference in Budapest, Hungary, 30 Sept. – 1 Oct. 2016, in 2000, China represented just 12 percent of global methanol demand, while North America and Western Europe represented 33 percent and 22 percent, respectively. By 2015, Chinese methanol consumption had grown to 54 percent of global demand while North American demand had fallen to 11 percent and Western Europe to 10 percent.

Chinese demand, Nash said, has grown significantly in traditional methanol derivatives, such as formaldehyde and acetic acid, but also in new end-uses, such as light olefins production, as well as expanded demand into energy applications, such as DME (dimethyl ether) and direct gasoline blending.

DME is primarily used as an aerosol propellant in the West, which represents a relatively small market overall. However, DME is also used in fuel applications—where it is mainly blended into liquefied petroleum gas (LPG). This application is widely used by Chinese consumers for home cooking and heating, which has helped drive methanol consumption into DME from virtually nothing in 2000, to the fourth largest methanol derivative in 2015, IHS Markit said.

China’s direct blending of methanol into the country’s gasoline pool has driven an average annual growth rate for this application of 25 percent from 2000 to 2015, making gasoline blending the third-largest methanol demand segment. A newer and rapidly growing demand segment for methanol (exclusively in China) is in the production of light olefins using methanol-to-olefins (MTO) technologies. In just four years, this end-use has driven staggering growth in methanol consumption and made MTO the sixth largest end-use for methanol. During the next few years, IHS Markit expects MTO to become the second largest end-use for methanol.

Feedstock costs for methanol comprise as much as 90 percent of the total cash-cost and, as such, access to low-cost feedstocks is key to methanol economics. The primary feedstock for methanol has been natural gas, representing as much as 85 percent of installed global capacity. Regions with access to low-cost natural gas have seen a surge in methanol capacity additions, including the Middle East, Africa and South America. With the growth in Chinese methanol demand and the country’s rich coal reserves, the industry has seen a sharp rise in coal-based methanol production.

Uncompetitive feedstock economics led to capacity rationalizations in North America and Europe in the early 2000s, with North American methanol capacity all but extinguished by 2008. However, recent exploitation of unconventional natural gas supplies in North America has allowed this region to regain its position as a methanol production powerhouse.

The sharp rise in North American production capacities and the cost position of these units has led to an increase in exports from the Americas that now add supply to both the European and Northeast Asian methanol markets. The expected growth in North American capacities will turn the region from a net importer to a net exporter by early 2019, IHS Markit said.

Supply and demand pressures have always driven methanol pricing, but now that methanol has significant volumes of derivatives that compete as alternatives to crude-oil derived products, the picture becomes significantly more complicated, since affordability of some methanol derivatives becomes dependent on crude oil price fluctuations, Nash said.

“Due to this linkage with crude oil markets, to assess the future direction of methanol demand, you have to assess not only the light olefins markets, but also the global fuel markets,” Nash said. ”With the drop in oil prices, methanol demand for these derivatives has been under pressure, with most consumers able to afford a much lower methanol price than in the past. This has been particularly the case for DME.”

The IHS Markit report said the methanol industry will face more moderate demand growth rates as direct-gasoline blending has matured and the feverish pace of MTO projects moderates. Overall demand during the next five years will grow at an average annual rate of almost 7 percent, with MTO becoming the second-largest methanol derivative. IHS Markit expects natural gas prices to remain below $5 U.S. per MMBtu in the next five years, and oil prices to rebound from the currently low level, the growing spread between these two commodities should therefore support methanol demand going forward.

To view the current agenda for the 34th Annual IHS World Methanol Conference, and to register for the event or training workshop, visit https://www.ihs.com/events/annual-wmc/register.html.