Terry Knowles, European Correspondent01.18.22

In December chemical industry leaders made an urgent appeal to the European Commission to cooperate in the development of an EU Chemical Industry Transition Pathway to sustain the extraordinary levels of investment that will be required by the EU’s chemical industry to fulfil the objectives of the EU’s Green Deal. This follows the publication of CEFIC’s first commissioned study into the business impacts of the EU Chemicals Strategy for Sustainability (CSS).

Perhaps unsurprisingly with the EU’s ambitious objectives of making Europe the cleanest continent when it comes to environmental matters, the results of the report demonstrate that there are enormous challenges ahead. Consequently CEFIC has invited EU policymakers and EU member state governments to cooperate in converting the CSS into a growth and innovation strategy.

European paint industry among those hit hardest

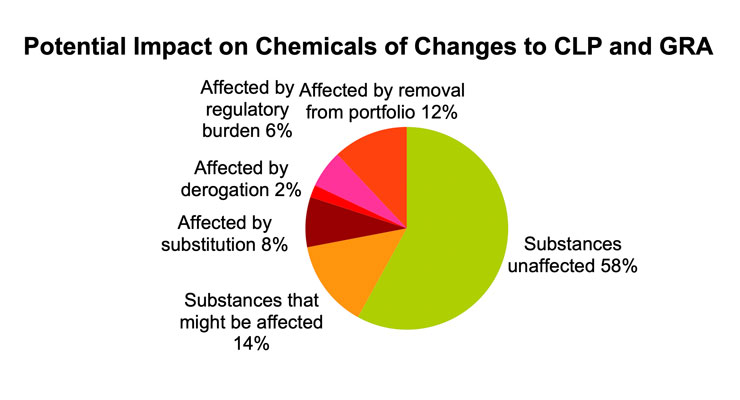

One of the findings from this first report is that something approaching 12,000 substances could fall into the two forthcoming legislative proposals alone, these being changes to Classification, Packaging and Labelling Regulation (CLP) and also the Generic Risk Approach (GRA). The approximately 12,000 different substances could count for 43% of the European chemical industry’s turnover. However, attempts to weight the significance of some substances over others in terms of the relative unknowns of definitions and criteria as part of the Chemicals Strategy for Sustainability, it could be that about 28% of the industry’s turnover might be affected. Of this, about a third of the substances might easily be substituted or reformulated.

The differing extents of the overall eventualities that may come to pass for the substances is illustrated by the pie chart, which effectively summarizes the quantitative findings of the report. Most concerning is the conclusion that 12% of the collective portfolio (which was based on information from more 100 different major chemical companies in Europe, that generate two-thirds of the collective industry turnover) could end up being removed. This would amount to the industry losing about €70 billion in turnover by 2040.

The qualitative findings of the report are that the impact on downstream users warrants further exploration. The analysis has shown that 74% of products in scope to be impacted by the addition of hazards to CLP and the extension of the GRA are professional or consumer products. The impacts on these products have been estimated and the results suggest that the downstream user sectors that could be most significantly impacted are:

• Polymer preparations and compounds, paper and board products, inks and toners, all of which may be used for food contact materials

• Paints and coatings

• Washing and cleaning products

• Adhesives and sealants

• Cosmetics and personal care products

• Lubricants and greases

• Biocidal products and plant protection products.

Dr. Martin Brudermueller, who is the president of CEFIC said, “The role of the chemical industry is to supply downstream customers with crucial materials to meet the targets of the Green Deal. The EU chemical industry is a major supplier of all manufacturing industries and essential and strategic value chains, including pharmaceuticals, electronics, EV batteries and construction materials. The intended policy changes coming with CSS will also create a significant ‘ripple effect’ across many value chains relying on chemicals.”

What is clear at this stage is that this is only the first report that has examined potential impacts of the EU Green Deal. What remains undetermined is how any changes will affect EU chemical exports, which will clearly bring a secondary layer impact. CEFIC’s second commissioned study is due to be published in the second quarter of 2022.

Industry in a state of transition

The proposed Transition Pathway that has been called for should incorporate timelines and measures for the chemical industry to develop substitutes and focus on those products where substitutes could be available first, which would be a relatively easy win on the basis of established approaches associated with risk assessments carried out under REACH. Furthermore, there will need to be more incentive to create markets for these new chemicals, along with a redoubling of efforts in terms of REACH enforcement and product safety legislation as far as imports are concerned. The package would also need to be complemented by a strong innovation agenda to speed the development of safe and sustainable-by-design alternatives. Finally, the Transition Pathway should also take into consideration the other transitions that the chemical industry is required to embrace, viz. climate neutrality, circularity and digitalization.

Major targets set for UK industry

The EU is not alone in setting ambitious targets for industry and across the English Channel, members of the British Coatings Federation (BCF) have joined other sectors in pledging to achieve net zero carbon emissions by 2050. The commitment was made at a recent BCF Board of Directors meeting and will be supported by more detailed Net Zero Roadmaps for each BCF sector.

The industry has also committed to a highly ambitious target for its paint recycling scheme, PaintCare. This scheme, which aims to create a circular economy for leftover decorative paint in the UK will aim to increase the percentage of leftover paint re-used, recycled, or re-manufactured from 2% today to 75% by 2030.

“I’m delighted the BCF Board has set ambitious targets for both Net Zero and leftover paint recycling, and we will be working hard with our members in the next 12 months to ensure a clear roadmap to achieve both objectives is in place,” said Tom Bowtell, CEO at the British Coatings Federation.

Sustainable production and recycling have been a key focus for the coatings industry in the UK since 1996 and are the basis for some of the 45 health, safety and environment key performance indicators monitored through the BCF’s Coatings Care program.

Latest Coatings Care figures showed record low levels of energy used in production as well as a significant decrease in production waste. 71% of production waste is now recycled, compared with just 17% in 1996. Accident rates are also at a record low and well below the latest UK Labour Force survey, with zero RIDDOR reported dangerous occurrences or fires at BCF member sites in 2020.

“We want to highlight and celebrate the work our members are doing to create a more sustainable industry. We have launched our #SustainableCoatings, #SustainableInks and #SustainableWallcoverings campaign, which will share case studies from our members showcasing what they have already done and what new initiatives they will be taking in future to increase sustainability. These will be shared on social media using the #SustainableCoatings and #SustainableInks hashtags on any related social media posts,” concluded Bowtell.

Perhaps unsurprisingly with the EU’s ambitious objectives of making Europe the cleanest continent when it comes to environmental matters, the results of the report demonstrate that there are enormous challenges ahead. Consequently CEFIC has invited EU policymakers and EU member state governments to cooperate in converting the CSS into a growth and innovation strategy.

European paint industry among those hit hardest

One of the findings from this first report is that something approaching 12,000 substances could fall into the two forthcoming legislative proposals alone, these being changes to Classification, Packaging and Labelling Regulation (CLP) and also the Generic Risk Approach (GRA). The approximately 12,000 different substances could count for 43% of the European chemical industry’s turnover. However, attempts to weight the significance of some substances over others in terms of the relative unknowns of definitions and criteria as part of the Chemicals Strategy for Sustainability, it could be that about 28% of the industry’s turnover might be affected. Of this, about a third of the substances might easily be substituted or reformulated.

The differing extents of the overall eventualities that may come to pass for the substances is illustrated by the pie chart, which effectively summarizes the quantitative findings of the report. Most concerning is the conclusion that 12% of the collective portfolio (which was based on information from more 100 different major chemical companies in Europe, that generate two-thirds of the collective industry turnover) could end up being removed. This would amount to the industry losing about €70 billion in turnover by 2040.

The qualitative findings of the report are that the impact on downstream users warrants further exploration. The analysis has shown that 74% of products in scope to be impacted by the addition of hazards to CLP and the extension of the GRA are professional or consumer products. The impacts on these products have been estimated and the results suggest that the downstream user sectors that could be most significantly impacted are:

• Polymer preparations and compounds, paper and board products, inks and toners, all of which may be used for food contact materials

• Paints and coatings

• Washing and cleaning products

• Adhesives and sealants

• Cosmetics and personal care products

• Lubricants and greases

• Biocidal products and plant protection products.

Dr. Martin Brudermueller, who is the president of CEFIC said, “The role of the chemical industry is to supply downstream customers with crucial materials to meet the targets of the Green Deal. The EU chemical industry is a major supplier of all manufacturing industries and essential and strategic value chains, including pharmaceuticals, electronics, EV batteries and construction materials. The intended policy changes coming with CSS will also create a significant ‘ripple effect’ across many value chains relying on chemicals.”

What is clear at this stage is that this is only the first report that has examined potential impacts of the EU Green Deal. What remains undetermined is how any changes will affect EU chemical exports, which will clearly bring a secondary layer impact. CEFIC’s second commissioned study is due to be published in the second quarter of 2022.

Industry in a state of transition

The proposed Transition Pathway that has been called for should incorporate timelines and measures for the chemical industry to develop substitutes and focus on those products where substitutes could be available first, which would be a relatively easy win on the basis of established approaches associated with risk assessments carried out under REACH. Furthermore, there will need to be more incentive to create markets for these new chemicals, along with a redoubling of efforts in terms of REACH enforcement and product safety legislation as far as imports are concerned. The package would also need to be complemented by a strong innovation agenda to speed the development of safe and sustainable-by-design alternatives. Finally, the Transition Pathway should also take into consideration the other transitions that the chemical industry is required to embrace, viz. climate neutrality, circularity and digitalization.

Major targets set for UK industry

The EU is not alone in setting ambitious targets for industry and across the English Channel, members of the British Coatings Federation (BCF) have joined other sectors in pledging to achieve net zero carbon emissions by 2050. The commitment was made at a recent BCF Board of Directors meeting and will be supported by more detailed Net Zero Roadmaps for each BCF sector.

The industry has also committed to a highly ambitious target for its paint recycling scheme, PaintCare. This scheme, which aims to create a circular economy for leftover decorative paint in the UK will aim to increase the percentage of leftover paint re-used, recycled, or re-manufactured from 2% today to 75% by 2030.

“I’m delighted the BCF Board has set ambitious targets for both Net Zero and leftover paint recycling, and we will be working hard with our members in the next 12 months to ensure a clear roadmap to achieve both objectives is in place,” said Tom Bowtell, CEO at the British Coatings Federation.

Sustainable production and recycling have been a key focus for the coatings industry in the UK since 1996 and are the basis for some of the 45 health, safety and environment key performance indicators monitored through the BCF’s Coatings Care program.

Latest Coatings Care figures showed record low levels of energy used in production as well as a significant decrease in production waste. 71% of production waste is now recycled, compared with just 17% in 1996. Accident rates are also at a record low and well below the latest UK Labour Force survey, with zero RIDDOR reported dangerous occurrences or fires at BCF member sites in 2020.

“We want to highlight and celebrate the work our members are doing to create a more sustainable industry. We have launched our #SustainableCoatings, #SustainableInks and #SustainableWallcoverings campaign, which will share case studies from our members showcasing what they have already done and what new initiatives they will be taking in future to increase sustainability. These will be shared on social media using the #SustainableCoatings and #SustainableInks hashtags on any related social media posts,” concluded Bowtell.