Terry Knowles, European Correspondent01.25.23

The New Year is always a good time to take stock of what has been happening and review some developments, collective fashion. This time I’m throwing the spotlight on paint companies that have been acquiring businesses in Europe, particularly with the emphasis across France, Germany, Italy and Poland. Poland is especially notable for being one of the two largest national markets in Eastern Europe (Turkiye being the other).

Looking deeper, there is potentially more to this now than mere sales. The picture of the European chemical sector is being redrawn from above with strategies for greater self-sufficiency, reduced dependency on outside supplies and potentially the redesign and emergence of new coatings technologies that are more eco-friendly and a lot of companies are going to have a much greater interest in Europe’s hotbed of eco-friendly coatings research. For businesses that claim to be passionate about preserving the planet, these grander ambitions for the European chemical sector are going to make it the place to be, because the greener design of chemicals is front and centre in Europe’s ambition of being the cleanest continent on the planet. In the coatings sector the development of new eco-friendly technologies built from the bottom up and based on renewable chemicals looks likely to pave the long-term way to a new set of environmentally friendly coatings technologies, probably over the next three decades.

The reality is that we hear very little about the greening of the chemical sector through sustainability and the circular economy in North America and even less from Asia Pacific, but Europe is streets ahead in this area. The acquisition of the Perstorp Group last year by Malaysia’s Petronas Chemicals Group highlights perfectly why European chemical companies with strong eco-credentials are so attractive and why there is so much interest in accessing their technologies. Players in Asian markets can see huge potential in technology transfer from acquired firms.

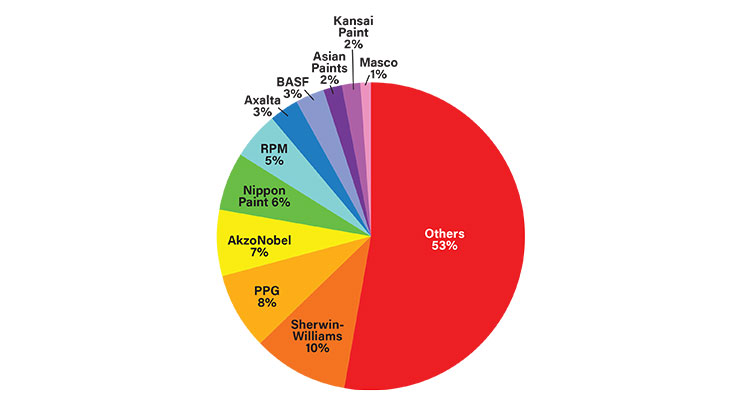

In recent years, Nippon Paint, Kansai Paint and PPG Industries have been the protagonists in buying up European coatings businesses, but lately Sherwin-Williams has rejoined the hunt, announcing a string of acquisitions based in Germany and Italy. The highly fragmented Italian paint and coatings sector offers up acquisitions not exactly regularly, but from time to time. On the other hand, the German paint industry, which has had a solid backbone of medium-sized paint and coatings companies, is also ideally placed for exports to surrounding economies, Germany having long been Europe’s top exporter of paint, of course.

In the December 2022 issue of CW I wrote on the topic of Kansai Paint’s strategy of targeting Europe for aggressive acquisitions, highlighting that in August it had acquired Westdeutsche Farben GmbH, a coatings manufacturer in Germany with specialist expertise in water-based coatings technology, which was added to a portfolio of coatings clustered around its Kansai Helios operations which encompassed its Rembrandtin railway coatings business. Since then, it has announced the takeover of Beckers’ global railway coatings business, which will significantly extend Kansai’s presence in Europe; the Becker Industrie SAS railway coatings business is based in France and will give Kansai Paint its first French subsidiary. The deal is expected to close in the first quarter of this year. Also in autumn 2022, Kansai acquired shares in CWS Lackfabrik in Germany, a powder coatings business. These acquisitions reflect a focus on business-to-business sales (industrial coatings) rather than business-to-consumer sales (decorative paints) and therefore a marked shift since the company’s exit from the African decorative paint operations, which it sold to AkzoNobel last year.

Sherwin-Williams is another company right at the forefront of European mergers and acquisitions activity in winter 2022/3 and most of its recent acquisitions trail can be traced through Germany and Italy. The gambit in Sherwin-Williams’ newest wave of acquisitions last year was its purchase of the industrial coatings business from Switzerland’s Sika. These coatings operations were actually based in Germany and fulfilled demand there and in Poland, Austria and Switzerland. The range of activities transferred included corrosion protection systems for civil infrastructure, engineering, energy and chemical sector applications as well as linings for tanks and pipes, waste and wastewater applications and fire protection systems for different construction materials. Not long after that, Sherwin-Williams acquired a German coatings formulator and distributor in a similar field: Gross & Perthun, which served the heavy equipment and transportation sectors and had a turnover of about US$50 million.

In autumn 2022 and in Germany again, Sherwin-Williams acquired Specialized Industrial Coatings Holding (SIC Holding), a Peter Möhrle Holding and GP Capital UG venture that held both Oskar Nolte GmbH and Klumpp Coatings GmbH. SIC Holding’s portfolio of solutions includes foil coatings as well as radiation-cured and water-based wood coatings for the board, furniture and flooring industries. This business served Europe, Asia and South America and the deal was expected to close in early 2023. Clearly an attractive option for moving further into the emerging markets there.

Meanwhile in Italy, Sherwin-Williams was to have acquired Industria Chimica Adriatica S.p.A. (ICA), a designer, manufacturer and distributor of industrial wood coatings used for kitchen cabinets, furniture and décor, building products, flooring and other speciality applications. The acquired business has a yearly turnover in excess of €150 million, with sales and operations globally, including production facilities in Italy and Poland, and ICA’s interest in the India-based joint venture, ICA Pidilite. The Italian wood finishes sector is very fragmented but slowly and surely many of the top players have been grabbed by multinationals wanting a slice of the action. This is another one of the top-flight companies that has been bought up by a multinational.

Finally, Nippon Paint’s most recent acquisitions in Europe counted among them Cromology from Wendel Investments, which positioned it especially well in the French and Italian decorative sectors and then the JUB Group, in Slovenia, which was seen as helping to build a bridge through the Eastern half of Europe that would eventually span across to its Turkish operations.

Why are companies targeting Europe?

Despite great uncertainty – and pressure – for industry, the mergers and acquisitions scene has continued to witness some selected activity in Europe, with the much wider EMEA regional market being the second-largest regional coatings market globally. The EMEA markets account for 30% of world paint and coatings demand, second only to Asia Pacific on 46% and ahead of North America on 19%. Regionally, that cannot be deemed insignificant.Looking deeper, there is potentially more to this now than mere sales. The picture of the European chemical sector is being redrawn from above with strategies for greater self-sufficiency, reduced dependency on outside supplies and potentially the redesign and emergence of new coatings technologies that are more eco-friendly and a lot of companies are going to have a much greater interest in Europe’s hotbed of eco-friendly coatings research. For businesses that claim to be passionate about preserving the planet, these grander ambitions for the European chemical sector are going to make it the place to be, because the greener design of chemicals is front and centre in Europe’s ambition of being the cleanest continent on the planet. In the coatings sector the development of new eco-friendly technologies built from the bottom up and based on renewable chemicals looks likely to pave the long-term way to a new set of environmentally friendly coatings technologies, probably over the next three decades.

The reality is that we hear very little about the greening of the chemical sector through sustainability and the circular economy in North America and even less from Asia Pacific, but Europe is streets ahead in this area. The acquisition of the Perstorp Group last year by Malaysia’s Petronas Chemicals Group highlights perfectly why European chemical companies with strong eco-credentials are so attractive and why there is so much interest in accessing their technologies. Players in Asian markets can see huge potential in technology transfer from acquired firms.

Who’s doing it and where are they?

While Europe often languishes at the bottom of the table in market research studies when it comes to annual growth in the paint and coatings sector, the global approach to “buying” market share gains in attractiveness for major paintmakers time and time again, especially when there own markets (such as USA and Japan) are mature. Regional players make attractive targets in growing market shares this way.In recent years, Nippon Paint, Kansai Paint and PPG Industries have been the protagonists in buying up European coatings businesses, but lately Sherwin-Williams has rejoined the hunt, announcing a string of acquisitions based in Germany and Italy. The highly fragmented Italian paint and coatings sector offers up acquisitions not exactly regularly, but from time to time. On the other hand, the German paint industry, which has had a solid backbone of medium-sized paint and coatings companies, is also ideally placed for exports to surrounding economies, Germany having long been Europe’s top exporter of paint, of course.

In the December 2022 issue of CW I wrote on the topic of Kansai Paint’s strategy of targeting Europe for aggressive acquisitions, highlighting that in August it had acquired Westdeutsche Farben GmbH, a coatings manufacturer in Germany with specialist expertise in water-based coatings technology, which was added to a portfolio of coatings clustered around its Kansai Helios operations which encompassed its Rembrandtin railway coatings business. Since then, it has announced the takeover of Beckers’ global railway coatings business, which will significantly extend Kansai’s presence in Europe; the Becker Industrie SAS railway coatings business is based in France and will give Kansai Paint its first French subsidiary. The deal is expected to close in the first quarter of this year. Also in autumn 2022, Kansai acquired shares in CWS Lackfabrik in Germany, a powder coatings business. These acquisitions reflect a focus on business-to-business sales (industrial coatings) rather than business-to-consumer sales (decorative paints) and therefore a marked shift since the company’s exit from the African decorative paint operations, which it sold to AkzoNobel last year.

Sherwin-Williams is another company right at the forefront of European mergers and acquisitions activity in winter 2022/3 and most of its recent acquisitions trail can be traced through Germany and Italy. The gambit in Sherwin-Williams’ newest wave of acquisitions last year was its purchase of the industrial coatings business from Switzerland’s Sika. These coatings operations were actually based in Germany and fulfilled demand there and in Poland, Austria and Switzerland. The range of activities transferred included corrosion protection systems for civil infrastructure, engineering, energy and chemical sector applications as well as linings for tanks and pipes, waste and wastewater applications and fire protection systems for different construction materials. Not long after that, Sherwin-Williams acquired a German coatings formulator and distributor in a similar field: Gross & Perthun, which served the heavy equipment and transportation sectors and had a turnover of about US$50 million.

In autumn 2022 and in Germany again, Sherwin-Williams acquired Specialized Industrial Coatings Holding (SIC Holding), a Peter Möhrle Holding and GP Capital UG venture that held both Oskar Nolte GmbH and Klumpp Coatings GmbH. SIC Holding’s portfolio of solutions includes foil coatings as well as radiation-cured and water-based wood coatings for the board, furniture and flooring industries. This business served Europe, Asia and South America and the deal was expected to close in early 2023. Clearly an attractive option for moving further into the emerging markets there.

Meanwhile in Italy, Sherwin-Williams was to have acquired Industria Chimica Adriatica S.p.A. (ICA), a designer, manufacturer and distributor of industrial wood coatings used for kitchen cabinets, furniture and décor, building products, flooring and other speciality applications. The acquired business has a yearly turnover in excess of €150 million, with sales and operations globally, including production facilities in Italy and Poland, and ICA’s interest in the India-based joint venture, ICA Pidilite. The Italian wood finishes sector is very fragmented but slowly and surely many of the top players have been grabbed by multinationals wanting a slice of the action. This is another one of the top-flight companies that has been bought up by a multinational.

Continuing the chain

Priorities and space preclude me from mentioning slightly older deals in too much detail but in the not too distant past PPG Industries acquired several businesses in Germany, mainly in the automotive coatings sector. These would be of interest for exploitation in the global automotive coatings industry which is far more extensively consolidated than the protective and wood coatings areas seen above. These deals included the takeover of Wörwag – a producer of liquid, powder and film coatings for the automotive sector; Cetelon – a manufacturer of wheel coatings for automotives and small trucks; and further in the past, Hemmelrath, a supplier of automotive coatings with participation in Germany, USA, China and Brazil.Finally, Nippon Paint’s most recent acquisitions in Europe counted among them Cromology from Wendel Investments, which positioned it especially well in the French and Italian decorative sectors and then the JUB Group, in Slovenia, which was seen as helping to build a bridge through the Eastern half of Europe that would eventually span across to its Turkish operations.