Charles W. Thurston, Latin America Correspondent12.07.20

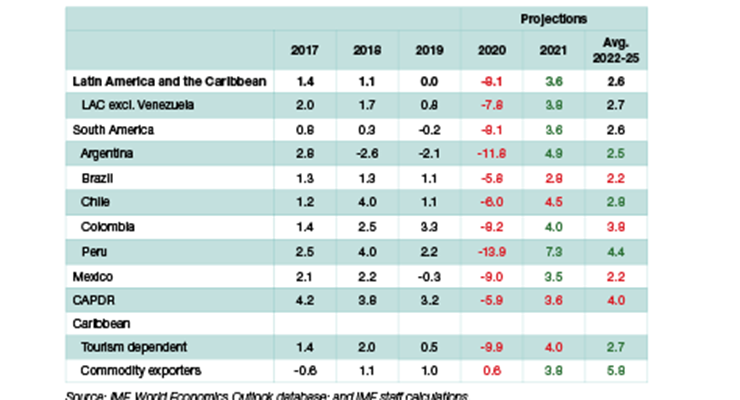

The cumulative impact of COVID-19 in Latin America shows that while some growth will occur in 2021, many countries will not recover until 2023, according to the International Monetary Fund. The IMF projects a real GDP contraction of 8.1 percent for 2020 in the region, according to its latest study.

“The pandemic, lockdowns, and external forces contributed to a historic collapse in activity in the second quarter of 2020. The LA5 countries experienced larger quarterly GDP contractions than in any recession on record,” the IMF said. The LA5 includes Brazil, Chile, Colombia, Mexico and Peru.

Regional economic collapses may set the stage for a rise in paint and coatings industry mergers and acquisitions, especially where a multinational company partners with a domestically-owned producer.

The IMF forecasts GDP growth in 2021 at 3.6 percent. However, most countries will not go back to pre-pandemic GDP until 2023; real income per capita will not return until 2025, later than any other region in the world, the IMF reckons.

New Cases in the Region

“COVID-19 has hit Latin America and the Caribbean harder than other parts of the world, both in human and economic terms. The relatively large human toll is evident: With only 8.2 percent of the world population, the region had 28 percent of cases and 34 percent of deaths, by end-September,” according to an Oct. 22 IMF blog by Samuel Pienknagura, Jorge Roldós and Alejandro Werner.

New cases continue to rise in some countries like Argentina, Costa Rica and Paraguay, while stabilizing in others like Brazil and Peru, per the IMF. The largest economies in the region – including Brazil, Chile, Mexico and Peru – have recorded some of the highest numbers of deaths per capita worldwide, according to an Oct. 20 IMF regional report, Western Hemisphere Pandemic Persistence Clouds the Recovery.

Compounding the impact, employment contracted more strongly than GDP in the second quarter of 2020, unlike in previous recessions, the IMF says. This employment contraction amounted to 20 percent on average for the five largest countries and up to 40 percent in Peru. Brazil, Chile, Colombia, Mexico, and Peru lost a combined 30 million jobs during the second quarter, the study found.

Uneven Impact Across the Region

While the overall impact of the crisis has been devastating to the national economies of the region, the degree of the impact has varied greatly country by country. While exports are down for many countries, the stabilized cost of oil, commodities and other import factors are making the trade balance less onerous for some, the IMF calculates.

“In countries such as the Dominican Republic, El Salvador, Paraguay and Uruguay, and in most of the Caribbean, a positive terms-of-trade (the ratio between a country’s export prices and its import prices) shock will partly compensate for the large negative external demand shock,” the IMF said. “In Bolivia, Colombia, and Ecuador, a negative terms-of-trade shock will add a further drag to growth.”

Brazil, Costa Rica and Uruguay experienced less pronounced contractions, and by July were back close to their January economic trends, the IMF found. Ecuador and Peru, experienced relatively large collapses and activity still remained subdued in July.

Several countries in Central America – including Panama and the Dominican Republic – were helped by a strong rebound in remittances and exports, together with low oil prices,

the study found.

Goods Demand Down, Corporate Debt Up

The internal demand for goods and services recovered in some countries but remains stagnant in others. “Retail sales and business confidence in Brazil bounced back and reached pre-COVID-19 levels in June, but in Mexico, they recovered less strongly and remain depressed,” the IMF reports.

The consumption of contact-intensive goods and services will likely be depressed until the pandemic is controlled, and income levels might stay subdued even afterward, the IMF study finds. “The resulting weak demand and uncertainty will hold investment back over the medium term. Some job losses might become permanent, reducing potential growth, especially where fiscal support has been timid,” the study says.

The long-term impact of this economic impact is profound, historically. “LAC’s real income per capita is expected to remain below pre-COVID-19 levels until 2025, which means that LAC faces the prospect of another lost decade, as in the 1980s,” the IMF warns.

Local Manufacturers Face Financial Strain

As a result of lower sales, manufacturers and other corporations in the region are at financial risk of bankruptcy. “The share of corporate debt at risk (when earnings are lower than interest expense), has doubled from 14 percent last December to 29 percent in June, and could rise more in 2021, in an adverse scenario,” the IMF suggests. “Debt restructuring will be critical to recovering the financial health of viable firms,” the study predicts.

Larger companies in the region have survived better than smaller companies. “The COVID-19 shock negatively affected many large corporations in LAC more than those in other regions. However, small and medium enterprises are expected to feel the largest effect,” the IMF finds. “In Brazil, firm surveys through August 2020 show that a higher fraction of small firms has reported declining sales than large firms.”

New investments will become an urgent factor in regional recovery. “Bankruptcies, firm closures, and the postponement of business plans because of weak demand and uncertainty will keep investment depressed over the medium term,” the IMF predicts. “The crisis will also lead to the destruction of organizational capital and relationship-specific capital between input suppliers and final goods producers, which is likely to amplify the effects of the crisis.”

Mergers and acquisitions in the paint and coatings industry are thus likely over the next two years, especially situations involving multinational companies that can partner with domestically-owned companies. While such M&A activity has focused on driving new growth within a global portfolio, the investments will need to be more strategic, with new sales planned over the longer-term. Apart from manufacturing, distribution and point-of-sales investments may be strong targets for multinational investors.

Overall foreign direct investment for all sectors in the region was bullish pre-COVID-19. In August 2019, the UN’s Economic Commission for Latin America and the Caribbean (ECLAC) found “in the region, FDI inflows were up by 13.2 percent year-on-year for the first time in five years, at $184.3 billion. This performance is explained by higher flows into just a few countries, however, mainly Brazil and Mexico.”

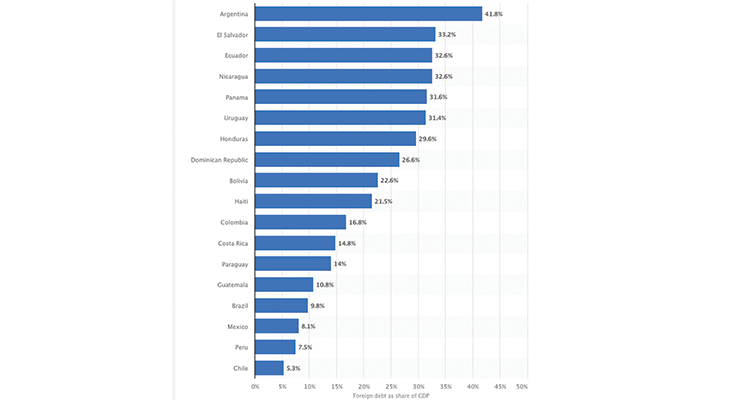

Future FDI flows may be more dependent on macro-economic policy than in the recent past. What remains to be seen is the degree to which multilateral recovery programs will assist national governments in the region to delay debt payments that help to permit increased domestic spending programs. Some countries like Argentina managed to renegotiate sovereign debt this year, while others remain in a fiscal quagmire. Ecuador, Uruguay and Colombia suffer double-digit debt as a percentage of GDP.

“The pandemic, lockdowns, and external forces contributed to a historic collapse in activity in the second quarter of 2020. The LA5 countries experienced larger quarterly GDP contractions than in any recession on record,” the IMF said. The LA5 includes Brazil, Chile, Colombia, Mexico and Peru.

Regional economic collapses may set the stage for a rise in paint and coatings industry mergers and acquisitions, especially where a multinational company partners with a domestically-owned producer.

The IMF forecasts GDP growth in 2021 at 3.6 percent. However, most countries will not go back to pre-pandemic GDP until 2023; real income per capita will not return until 2025, later than any other region in the world, the IMF reckons.

New Cases in the Region

“COVID-19 has hit Latin America and the Caribbean harder than other parts of the world, both in human and economic terms. The relatively large human toll is evident: With only 8.2 percent of the world population, the region had 28 percent of cases and 34 percent of deaths, by end-September,” according to an Oct. 22 IMF blog by Samuel Pienknagura, Jorge Roldós and Alejandro Werner.

New cases continue to rise in some countries like Argentina, Costa Rica and Paraguay, while stabilizing in others like Brazil and Peru, per the IMF. The largest economies in the region – including Brazil, Chile, Mexico and Peru – have recorded some of the highest numbers of deaths per capita worldwide, according to an Oct. 20 IMF regional report, Western Hemisphere Pandemic Persistence Clouds the Recovery.

Compounding the impact, employment contracted more strongly than GDP in the second quarter of 2020, unlike in previous recessions, the IMF says. This employment contraction amounted to 20 percent on average for the five largest countries and up to 40 percent in Peru. Brazil, Chile, Colombia, Mexico, and Peru lost a combined 30 million jobs during the second quarter, the study found.

Uneven Impact Across the Region

While the overall impact of the crisis has been devastating to the national economies of the region, the degree of the impact has varied greatly country by country. While exports are down for many countries, the stabilized cost of oil, commodities and other import factors are making the trade balance less onerous for some, the IMF calculates.

“In countries such as the Dominican Republic, El Salvador, Paraguay and Uruguay, and in most of the Caribbean, a positive terms-of-trade (the ratio between a country’s export prices and its import prices) shock will partly compensate for the large negative external demand shock,” the IMF said. “In Bolivia, Colombia, and Ecuador, a negative terms-of-trade shock will add a further drag to growth.”

Brazil, Costa Rica and Uruguay experienced less pronounced contractions, and by July were back close to their January economic trends, the IMF found. Ecuador and Peru, experienced relatively large collapses and activity still remained subdued in July.

Several countries in Central America – including Panama and the Dominican Republic – were helped by a strong rebound in remittances and exports, together with low oil prices,

the study found.

Goods Demand Down, Corporate Debt Up

The internal demand for goods and services recovered in some countries but remains stagnant in others. “Retail sales and business confidence in Brazil bounced back and reached pre-COVID-19 levels in June, but in Mexico, they recovered less strongly and remain depressed,” the IMF reports.

The consumption of contact-intensive goods and services will likely be depressed until the pandemic is controlled, and income levels might stay subdued even afterward, the IMF study finds. “The resulting weak demand and uncertainty will hold investment back over the medium term. Some job losses might become permanent, reducing potential growth, especially where fiscal support has been timid,” the study says.

The long-term impact of this economic impact is profound, historically. “LAC’s real income per capita is expected to remain below pre-COVID-19 levels until 2025, which means that LAC faces the prospect of another lost decade, as in the 1980s,” the IMF warns.

Local Manufacturers Face Financial Strain

As a result of lower sales, manufacturers and other corporations in the region are at financial risk of bankruptcy. “The share of corporate debt at risk (when earnings are lower than interest expense), has doubled from 14 percent last December to 29 percent in June, and could rise more in 2021, in an adverse scenario,” the IMF suggests. “Debt restructuring will be critical to recovering the financial health of viable firms,” the study predicts.

Larger companies in the region have survived better than smaller companies. “The COVID-19 shock negatively affected many large corporations in LAC more than those in other regions. However, small and medium enterprises are expected to feel the largest effect,” the IMF finds. “In Brazil, firm surveys through August 2020 show that a higher fraction of small firms has reported declining sales than large firms.”

New investments will become an urgent factor in regional recovery. “Bankruptcies, firm closures, and the postponement of business plans because of weak demand and uncertainty will keep investment depressed over the medium term,” the IMF predicts. “The crisis will also lead to the destruction of organizational capital and relationship-specific capital between input suppliers and final goods producers, which is likely to amplify the effects of the crisis.”

Mergers and acquisitions in the paint and coatings industry are thus likely over the next two years, especially situations involving multinational companies that can partner with domestically-owned companies. While such M&A activity has focused on driving new growth within a global portfolio, the investments will need to be more strategic, with new sales planned over the longer-term. Apart from manufacturing, distribution and point-of-sales investments may be strong targets for multinational investors.

Overall foreign direct investment for all sectors in the region was bullish pre-COVID-19. In August 2019, the UN’s Economic Commission for Latin America and the Caribbean (ECLAC) found “in the region, FDI inflows were up by 13.2 percent year-on-year for the first time in five years, at $184.3 billion. This performance is explained by higher flows into just a few countries, however, mainly Brazil and Mexico.”

Future FDI flows may be more dependent on macro-economic policy than in the recent past. What remains to be seen is the degree to which multilateral recovery programs will assist national governments in the region to delay debt payments that help to permit increased domestic spending programs. Some countries like Argentina managed to renegotiate sovereign debt this year, while others remain in a fiscal quagmire. Ecuador, Uruguay and Colombia suffer double-digit debt as a percentage of GDP.