Gary Shawhan, Chemark Consulting02.02.24

The Southeast Asia region, with its ready access to global shipping corridors, is ideally suited to support the global supply chain. The region contains a number of countries that have an emerging economy and a young, energetic work force that supports the profile of a low-cost manufacturer.

China has been the leader in the global supply chain for more than 20 years. Today, however, China’s leadership role is in transition with an uncertain outcome. India, as the second largest economy in the SE Asia region, is emerging as an attractive alternative to China as a primary supply chain hub. This article explores the reasons behind China’s demise and the emerging role India can play in a revised global supply chain in SE Asia region.

Eventually, certain issues could not be ignored. In particular, China trade practices were creating long-term problems for their global export customers with their competitive position in certain markets. They also began to reveal underlying risks involved in reliance on China as a primary source (or sole source) of supply.

These issues included tariff inequities, rising labor costs and the impact of the pandemic on supply and China’s approach to dealing with this problem.

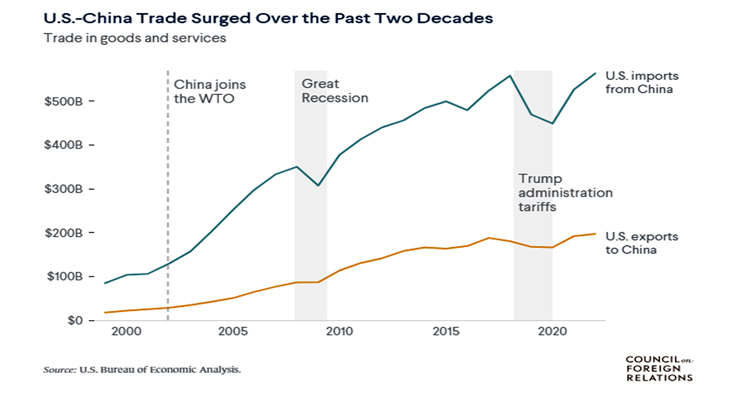

• China has been the largest trading partner with the United States for more than 20 years. The trade imbalance between the U.S. and China had grown steadily over this time period. In 2018, it was -$420B or 78% of the net import/export value between the two countries.

The Chinese impose significant tariffs on imports of good from the U.S. and other foreign countries. The U.S. (and other importing countries as well) left this issue largely unaddressed and un-challenged as they benefited from the low costs of imported goods. Its impact was amplified by the fact that similar import tariffs had not been put in place by foreign governments to level the playing field.

In select markets subsidization of both new plant construction and operational costs by the Chinese government made it difficult for offshore companies to justify in-country, new plant construction. This dynamic allowed China to build a powerful manufacturing infrastructure cementing their leading role in the supply chain.

In addition, new plant construction incorporated state-of-the-art technology further improving China’s competitive advantage. Market examples include appliance, automotive/transportation, electronics and steel or aluminum.

In 2018, the U.S. announced new tariffs and established quotas on certain imported goods. The consequence of these actions was increased confrontational dialogue between the U.S. and China on trade policy. It also drew attention to one of the consequences resulting from the existing level of dependence on sourcing from China.

• The labor cost advantage that China enjoyed early in its growth cycle slowly began to diminish as salaries for workers started to normalize with the international marketplace. This economic evolution began altering China’s traditional behavior as the supply chain leader.

This escalation of the income for the average Chinese worker was reflected in the emergence of a growing middle class. This transition created significant growth in demand for goods and services in-country. This demand was now competing with China’s traditional global export business.

• The pandemic brought into focus the vulnerable position most companies and supply chain management teams had put themselves in regarding sourcing dependence. Its impact was wide ranging and included: Customer allocations; force majeure on certain contracts with major accounts; significant price increases for many raw materials; and elimination or consolidation of certain product lines to address critical shortages.

The pandemic underscored the strong control that the Chinese government had over all companies manufacturing goods and services within their country. Unexpected plant shut-downs, lockdowns, and supply allocations favoring Chinese companies revealed one of the risks associated with doing business in a country with an authoritarian government. Import customers that had relied heavily on sourcing from China were left extremely vulnerable to policy change.

Collectively, these issues have resulted in a reappraisal of business strategies involving China by many organizations. China has opened the door for India along with other SE Asia countries to provide a viable alternative to China long-standing dominance as the leader in the global supply chain.

• China economy (post-COVID) has not returned to its prior levels. Decline in exports numbers to the U.S. and Europe is evident. At all levels, government debt is limiting efforts to prop-up the economy.

• Concern over protection of strategic IP by the U.S. and other countries has taken on a high level of priority. Evidence of IP theft, espionage and loss of critical technology related to defense have surfaced.

• Territorial expansion by the Chinese government throughout SE Asia is being aggressively pursued. Regional threats including military provocations have increased exponentially.

• China‘s struggling economy is in part paying the price for subsidizing industry to maintain economic growth. This includes under-writing residential and commercial building project that were not needed.

• China’s recent geopolitical alignments with countries such as Russia,

Iran and North Korea has created red flags for future foreign investments within China.

China has been the leader in the global supply chain for more than 20 years. Today, however, China’s leadership role is in transition with an uncertain outcome. India, as the second largest economy in the SE Asia region, is emerging as an attractive alternative to China as a primary supply chain hub. This article explores the reasons behind China’s demise and the emerging role India can play in a revised global supply chain in SE Asia region.

China – The Ides of Change

China built their position as a global supply chain leader by aggressively supporting foreign investments while taking advantage of their large workforce and low manufacturing costs. As their supply position grew, issues emerged in doing business with China. These issues were easy to ignore (or put aside) during the period when things were working well.Eventually, certain issues could not be ignored. In particular, China trade practices were creating long-term problems for their global export customers with their competitive position in certain markets. They also began to reveal underlying risks involved in reliance on China as a primary source (or sole source) of supply.

These issues included tariff inequities, rising labor costs and the impact of the pandemic on supply and China’s approach to dealing with this problem.

• China has been the largest trading partner with the United States for more than 20 years. The trade imbalance between the U.S. and China had grown steadily over this time period. In 2018, it was -$420B or 78% of the net import/export value between the two countries.

The Chinese impose significant tariffs on imports of good from the U.S. and other foreign countries. The U.S. (and other importing countries as well) left this issue largely unaddressed and un-challenged as they benefited from the low costs of imported goods. Its impact was amplified by the fact that similar import tariffs had not been put in place by foreign governments to level the playing field.

In select markets subsidization of both new plant construction and operational costs by the Chinese government made it difficult for offshore companies to justify in-country, new plant construction. This dynamic allowed China to build a powerful manufacturing infrastructure cementing their leading role in the supply chain.

In addition, new plant construction incorporated state-of-the-art technology further improving China’s competitive advantage. Market examples include appliance, automotive/transportation, electronics and steel or aluminum.

In 2018, the U.S. announced new tariffs and established quotas on certain imported goods. The consequence of these actions was increased confrontational dialogue between the U.S. and China on trade policy. It also drew attention to one of the consequences resulting from the existing level of dependence on sourcing from China.

• The labor cost advantage that China enjoyed early in its growth cycle slowly began to diminish as salaries for workers started to normalize with the international marketplace. This economic evolution began altering China’s traditional behavior as the supply chain leader.

This escalation of the income for the average Chinese worker was reflected in the emergence of a growing middle class. This transition created significant growth in demand for goods and services in-country. This demand was now competing with China’s traditional global export business.

• The pandemic brought into focus the vulnerable position most companies and supply chain management teams had put themselves in regarding sourcing dependence. Its impact was wide ranging and included: Customer allocations; force majeure on certain contracts with major accounts; significant price increases for many raw materials; and elimination or consolidation of certain product lines to address critical shortages.

The pandemic underscored the strong control that the Chinese government had over all companies manufacturing goods and services within their country. Unexpected plant shut-downs, lockdowns, and supply allocations favoring Chinese companies revealed one of the risks associated with doing business in a country with an authoritarian government. Import customers that had relied heavily on sourcing from China were left extremely vulnerable to policy change.

Recent Events Impacting China’s Future Supply Chain Position

Recent events and actions by the Chinese government have significantly amplified the concerns of foreign governments and foreign manufacturers about reliance on China for supply. Table 1 offers a summary of recent events and actions.Collectively, these issues have resulted in a reappraisal of business strategies involving China by many organizations. China has opened the door for India along with other SE Asia countries to provide a viable alternative to China long-standing dominance as the leader in the global supply chain.

Table 1. Recent Events and Activities Impacting China Relations with Key Export Countries

• China has increasingly exercised their authoritarian control over businesses operating within China. The unpredictability of their actions has brought added risk to companies doing business there.• China economy (post-COVID) has not returned to its prior levels. Decline in exports numbers to the U.S. and Europe is evident. At all levels, government debt is limiting efforts to prop-up the economy.

• Concern over protection of strategic IP by the U.S. and other countries has taken on a high level of priority. Evidence of IP theft, espionage and loss of critical technology related to defense have surfaced.

• Territorial expansion by the Chinese government throughout SE Asia is being aggressively pursued. Regional threats including military provocations have increased exponentially.

• China‘s struggling economy is in part paying the price for subsidizing industry to maintain economic growth. This includes under-writing residential and commercial building project that were not needed.

• China’s recent geopolitical alignments with countries such as Russia,

Iran and North Korea has created red flags for future foreign investments within China.

Table 2. GDP and Growth Rate for Leading Global Economy’s

| Rank | Country | GDP (2023) | Annual Growth Rate |

| 1 | United States | $23.7 trillion | 1.6% |

| 2 | China | $17.7 trillion | 5.0% |

| 3 | Japan | $4.9 trilion | 1.3% |

| 4 | Germany | $4.3 trillion | 0.2% |

| 5 | India | $3.7 trillion | 7.2% |