Sean Milmo, European Correspondent09.03.19

Europe’s economies are suffering from the impact of a global economic downturn.

But for European coatings producers, it is an opportunity to show how well they have been reorganizing themselves to cope with economic pressures.

Demand for coatings in the first half of this year has been static or has even declined in some sectors.

But while coatings businesses have been recording decreases in volume sales or at best small rises, at home and abroad, their profits have been increasing, in some cases at double-digit levels.

Coatings companies are seeing the benefits of adopting strategies focused on improving margins through streamlining portfolios in favor of premium products, introducing cost-cutting programs and implementing operational efficiencies.

While economic analysts are predicting slower economic growth this year both in Europe and globally, coatings companies are expecting that 2019 will be for them a year of sluggish sales growth but of greater profitability.

The economic and financial affairs directorate of the European Commission, the European Union’s Brussels-based executive, has in its forecast for this summer predicted that the EU’s GDP growth this year will drop to 1.2 percent compared to 1.9 percent in 2018.

It blames the slowdown on factors like trade frictions, such as tensions between the U.S. and China, and protracted weakness in global industrial output. An EU industrial confidence index, based on company surveys, has shown its biggest decrease in around eight years.

Much of this slump in confidence has been due to difficulties in Germany’s export-orientated economy, whose output dropped by 0.1 percent in the second quarter compared to the previous three months.

This fall helped to halve the growth rate of the 19-country eurozone to 0.2 percent in the second quarter.

Germany is Europe’s economic stronghold, as well as having the largest coatings sector, which exports almost three times as many coatings products by value as it imports.

Much of the slowdown in Europe has been in its western countries while GDP in central and eastern European countries has continued to grow relatively strongly with thriving coatings sectors.

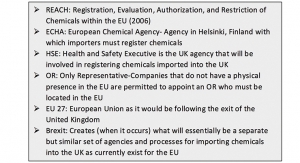

Coatings businesses in the UK have also appeared to be doing well despite uncertainties about Brexit with the country’s departure from the EU being postponed in late March to the end of October 2019.

The UK economy shrank by 0.2 percent between April and June this year the first time it has contracted since 2012.

Usually, the UK coatings sector follows trends in GDP so that when domestic output decreases that of coatings will as well, often together with sales.

In fact so far this year it has been the opposite. UK decorative sales went up by five percent by volume and eight percent by value in the first half of 2017, in contrast to annual declining or flat sales in 2017 and 2018.

‘’It’s the stockpiling effect of Brexit,’’ said Tom Bowtell, chief executive of the British Coatings Federation (BCF). “Companies are worried about post-Brexit tariffs and customs delays.’’

Once Brexit takes place supply chain difficulties may become a problem in certain markets, particularly in northern Europe, because the UK is currently a European hub for supplies of finished products and raw materials.

In the UK itself, 84 percent of imports of coatings and inks come from the rest of Europe, according to BCF figures.

However, for much of Europe, the main current challenge has been to offset slowdowns or declines in volume sales, triggered by the present economic downturn, with price increases and cost reductions in production and other operations.

Among the European coatings multinationals AkzoNobel, the European market leader in decorative and key industrial coatings sectors, offset in the first half of 2019 flat or lower sales revenues with higher operating income.

Adjusted operating income went up by 25 percent in the second quarter while in the first half it rose by 36 percent.

The company, which has over 40 percent of sales in Europe and much of the rest in the Asia Pacific, has been focusing on price mix initiatives, covering prices, discounts and credit, to guard against volume sales reductions by using price increases to exploit the value of its premium products.

In its decorative business, a five percent volume sales decline in the first half, mainly caused by a decrease in China, was offset by a five percent price-mix rise.

There was a similar strategy in performance coatings where a volume decline was mostly compensated by a six percent price-mix increase.

The company is striving to achieve an average 15 percent return on sales (ROS) by 2020.

In the second quarter the decorative ROS was 13.5 percent against 12.2 percent in the same period in 2018 and in performance coatings the ROS was 13.6 percent against 11.8 percent.

BASF finished coatings behind AkzoNobel in terms of sales, but also a leading raw materials supplier, has been following a similar strategy of compensating for volume sales declines through price rises and cost controls.

The company has been hit this year by a slowdown in automotive sales in Europe and the rest of the world.

In the first half global automotive output declined by six percent while the car market in China, a major outlet for BASF, decreased by 13 percent, according to the company.

Nonetheless, the company was able to implement “significant” prices increases in coatings, which helped it to achieve a seven percent rise in EBITDA (earnings before interest, taxes, depreciation and amortization) in its surface technologies segment which includes its coatings business.

Similar objectives are being followed by coating companies which are serving regional markets in Europe.

Finland-based Tikkurila, the market leader in northeastern Europe covering Scandinavia, Poland and Russia as well as having a presence in Central Asia and China, reported a 25 percent rise in adjusted operating profit in the first half while revenue went down by 1.7 percent.

‘’Tikkurila is focusing on premium brands, and prioritizing value over volume,’’ said Elisa Markula, the company’s chief executive.

‘’In Russia and Poland, growth is fueled by the increasing demand for premium products, which is positively reflected in our sales mix. The (combined) price increases and positive development in our sales mix partly offset decreased volumes.’’

European coatings companies are hoping that in addition to their ability to provide innovative, premium products, lower raw materials costs due to softer oil prices will continue to help them broaden margins for at least the next few years.

But for European coatings producers, it is an opportunity to show how well they have been reorganizing themselves to cope with economic pressures.

Demand for coatings in the first half of this year has been static or has even declined in some sectors.

But while coatings businesses have been recording decreases in volume sales or at best small rises, at home and abroad, their profits have been increasing, in some cases at double-digit levels.

Coatings companies are seeing the benefits of adopting strategies focused on improving margins through streamlining portfolios in favor of premium products, introducing cost-cutting programs and implementing operational efficiencies.

While economic analysts are predicting slower economic growth this year both in Europe and globally, coatings companies are expecting that 2019 will be for them a year of sluggish sales growth but of greater profitability.

The economic and financial affairs directorate of the European Commission, the European Union’s Brussels-based executive, has in its forecast for this summer predicted that the EU’s GDP growth this year will drop to 1.2 percent compared to 1.9 percent in 2018.

It blames the slowdown on factors like trade frictions, such as tensions between the U.S. and China, and protracted weakness in global industrial output. An EU industrial confidence index, based on company surveys, has shown its biggest decrease in around eight years.

Much of this slump in confidence has been due to difficulties in Germany’s export-orientated economy, whose output dropped by 0.1 percent in the second quarter compared to the previous three months.

This fall helped to halve the growth rate of the 19-country eurozone to 0.2 percent in the second quarter.

Germany is Europe’s economic stronghold, as well as having the largest coatings sector, which exports almost three times as many coatings products by value as it imports.

Much of the slowdown in Europe has been in its western countries while GDP in central and eastern European countries has continued to grow relatively strongly with thriving coatings sectors.

Coatings businesses in the UK have also appeared to be doing well despite uncertainties about Brexit with the country’s departure from the EU being postponed in late March to the end of October 2019.

The UK economy shrank by 0.2 percent between April and June this year the first time it has contracted since 2012.

Usually, the UK coatings sector follows trends in GDP so that when domestic output decreases that of coatings will as well, often together with sales.

In fact so far this year it has been the opposite. UK decorative sales went up by five percent by volume and eight percent by value in the first half of 2017, in contrast to annual declining or flat sales in 2017 and 2018.

‘’It’s the stockpiling effect of Brexit,’’ said Tom Bowtell, chief executive of the British Coatings Federation (BCF). “Companies are worried about post-Brexit tariffs and customs delays.’’

Once Brexit takes place supply chain difficulties may become a problem in certain markets, particularly in northern Europe, because the UK is currently a European hub for supplies of finished products and raw materials.

In the UK itself, 84 percent of imports of coatings and inks come from the rest of Europe, according to BCF figures.

However, for much of Europe, the main current challenge has been to offset slowdowns or declines in volume sales, triggered by the present economic downturn, with price increases and cost reductions in production and other operations.

Among the European coatings multinationals AkzoNobel, the European market leader in decorative and key industrial coatings sectors, offset in the first half of 2019 flat or lower sales revenues with higher operating income.

Adjusted operating income went up by 25 percent in the second quarter while in the first half it rose by 36 percent.

The company, which has over 40 percent of sales in Europe and much of the rest in the Asia Pacific, has been focusing on price mix initiatives, covering prices, discounts and credit, to guard against volume sales reductions by using price increases to exploit the value of its premium products.

In its decorative business, a five percent volume sales decline in the first half, mainly caused by a decrease in China, was offset by a five percent price-mix rise.

There was a similar strategy in performance coatings where a volume decline was mostly compensated by a six percent price-mix increase.

The company is striving to achieve an average 15 percent return on sales (ROS) by 2020.

In the second quarter the decorative ROS was 13.5 percent against 12.2 percent in the same period in 2018 and in performance coatings the ROS was 13.6 percent against 11.8 percent.

BASF finished coatings behind AkzoNobel in terms of sales, but also a leading raw materials supplier, has been following a similar strategy of compensating for volume sales declines through price rises and cost controls.

The company has been hit this year by a slowdown in automotive sales in Europe and the rest of the world.

In the first half global automotive output declined by six percent while the car market in China, a major outlet for BASF, decreased by 13 percent, according to the company.

Nonetheless, the company was able to implement “significant” prices increases in coatings, which helped it to achieve a seven percent rise in EBITDA (earnings before interest, taxes, depreciation and amortization) in its surface technologies segment which includes its coatings business.

Similar objectives are being followed by coating companies which are serving regional markets in Europe.

Finland-based Tikkurila, the market leader in northeastern Europe covering Scandinavia, Poland and Russia as well as having a presence in Central Asia and China, reported a 25 percent rise in adjusted operating profit in the first half while revenue went down by 1.7 percent.

‘’Tikkurila is focusing on premium brands, and prioritizing value over volume,’’ said Elisa Markula, the company’s chief executive.

‘’In Russia and Poland, growth is fueled by the increasing demand for premium products, which is positively reflected in our sales mix. The (combined) price increases and positive development in our sales mix partly offset decreased volumes.’’

European coatings companies are hoping that in addition to their ability to provide innovative, premium products, lower raw materials costs due to softer oil prices will continue to help them broaden margins for at least the next few years.