Terry Knowles, European Correspondent09.06.21

The extremely disruptive pandemic conditions of early 2020 generated strange-looking repercussions in the interim results posted in the summer of last year.

For those companies that are diversified enough to enjoy exposure to both the decorative markets and the full panoply of industrial coatings segments, excessive growth in the former (especially DIY) partially compensated for demand collapses in most of the latter. Those serving the industrial coatings sector only were not so lucky. Very alarming double-digit collapses in sales had been reported, to use the industry’s own vernacular.

This summer, the interim results posted in late July and August showed a more comprehensive return to growth as industry begins to re-establish its old trading patterns wherever possible. This article highlights some of the results, views and trends that have been reported on Europe during the second quarter and the greater first six months.

Reports from inside Europe

The higher the climb, the better the view! So with AkzoNobel as the European leader, some of the most detailed insights are made possible. Latest figures from AkzoNobel show that 51% of its turnover is derived in the EMEA region (see chart of AkzoNobel’s sales).

Throughout the first half of 2021, AkzoNobel’s Decorative Paints business recorded a 17% increase in turnover in the EMEA region to reach an interim total of €1,316 million. In the second quarter alone, when the passion for DIY usually reignites, there was a 13% increase in EMEA sales to €720 million. Across the EMEA region, this was attributed to strong demand from both the professional and DIY segments, with volume sales up significantly. Although pricing trends were positive in the region, the company’s price mix was impacted by strong growth in areas where average selling prices for paint are lower, viz. the Middle East and Africa.

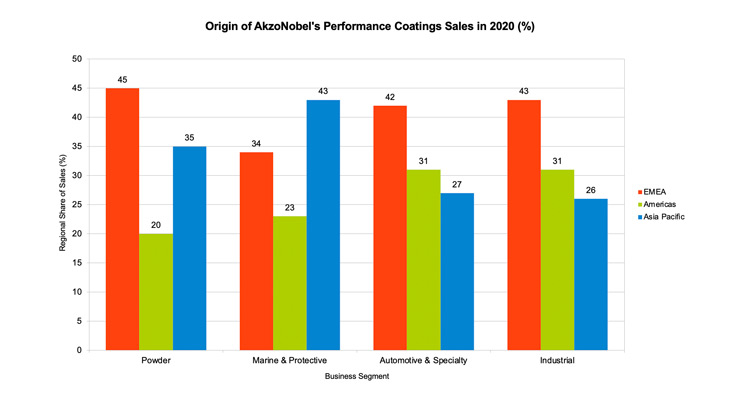

In AkzoNobel’s Performance Coatings business, where its industrial coatings portfolio resides, the figures point to growth across the board. Here, the EMEA region is the largest contributor to sales in three of the four reporting segments, the exception being the Marine & Protective business, which is more naturally dominated by the strength of the Asian markets. The relative strengths of each region in terms of their contribution for 2020 are given in the bar chart. Hence the relative strengths of each region provide a background for understanding the following recoveries by segment as set out in the company’s interim report:

• Powder Coatings’ sales in the first half of 2021 rose by 29% and by 48% in second quarter alone. AkzoNobel enjoyed both demand and market share growth in this area, driven mainly by rising consumption from the automotive sector.

• Turnover in the Industrial Coatings operations grew by 16% in the first half and by 26% in the second quarter. There was growth in all sub-segments of the Industrial Coatings business in the second quarter, but particularly packaging coatings, which have performed consistently well during the pandemic conditions.

• In the Automotive & Specialty Coatings segment, vehicle refinishes continued to recover and aerospace coatings continued on their sequential quarterly path to recovery. The aerospace sector came good for AkzoNobel in terms of maintenance and repair. In the Automotive & Specialty Coatings segment, the second quarter registered a 39% increase in sales, which contributed to a 14% increase in sales in the first half of 2021 over 2020.

• Finally, the Marine & Protective operations that have a greater strength in the Asia Pacific region have seen the slowest return to growth, posting a 16% increase in sales in the second quarter, thereby contributing to 4% growth in the first half of the year. One of the strengths in this business was yacht coatings operations.

Tikkurila, which I profiled in the June 2021 issue of CW to highlight the scope of PPG’s acquisition, is also a key regional player based in Northern Europe, with special exposure to the markets of Scandinavia and the Baltic states. Russia and Sweden are its largest markets, taking 23% each, followed by Finland and Poland, which take a further 17% and 16% respectively.

Decorative paints constitute the vast majority of its business (84%), while industrial coatings operations covering the wood, protective and some OEM applications comprise the other 16%.

Revenues at Tikkurila rose by 7.4% in the second quarter of 2021, contributing to an increase of 8.3% for the first half of the year. Surprisingly, operating profits at the company were affected by costs – as measured across both periods – as a result of PPG’s tender offer.

Nevertheless, Tikkurila experienced good revenue growth in decorative paints in both the interior and exterior sub-segments. Revenue grew in all key geographies, except for Finland, where the second quarter revenue was slightly below the comparison period. Industrial paint revenues grew in both the metal and wood paints areas, when compared to the same time last year.

Among some of the key points for Tikkurila at the half-way stage in the year, the company’s interim CEO Markus Melkko said, “During the first half of the year, the global paint industry has experienced an unprecedented raw material disruption, which has further escalated during the second quarter. The raw material and packaging inflation impacted our cost basis, and the simultaneous raw material supply issues impacted our ability to serve our customers... Tikkurila experienced good revenue growth in decorative paints in both interior and exterior paints. Revenue grew in all key geographies, except in Finland, where the second quarter revenue was slightly below the comparison period. Industrial paint revenue grew in both metal and wood paints against the comparison period... We expect that raw material inflation and some supply constraints will continue during the second half of 2021. We will maintain focus on serving our customers to the best of our capabilities under the supply constraints, while maintaining our profitability with smart margin management and targeted pricing changes to offset inflation.”

Reports from Outside Europe

• PPG is AkzoNobel’s closest competitor in the EMEA region. Its architectural coatings activities are usually singled out for performance highlights when results are reported.

For the quarter ending with June 2021, PPG said that year-on-year net sales, excluding the impact of currency and acquisitions (organic sales), increased by a mid-teen percentage. The company reported sequential softening in the DIY paint segment, but this was more than offset by strong demand for architectural trade products.

For those companies that are diversified enough to enjoy exposure to both the decorative markets and the full panoply of industrial coatings segments, excessive growth in the former (especially DIY) partially compensated for demand collapses in most of the latter. Those serving the industrial coatings sector only were not so lucky. Very alarming double-digit collapses in sales had been reported, to use the industry’s own vernacular.

This summer, the interim results posted in late July and August showed a more comprehensive return to growth as industry begins to re-establish its old trading patterns wherever possible. This article highlights some of the results, views and trends that have been reported on Europe during the second quarter and the greater first six months.

Reports from inside Europe

The higher the climb, the better the view! So with AkzoNobel as the European leader, some of the most detailed insights are made possible. Latest figures from AkzoNobel show that 51% of its turnover is derived in the EMEA region (see chart of AkzoNobel’s sales).

Throughout the first half of 2021, AkzoNobel’s Decorative Paints business recorded a 17% increase in turnover in the EMEA region to reach an interim total of €1,316 million. In the second quarter alone, when the passion for DIY usually reignites, there was a 13% increase in EMEA sales to €720 million. Across the EMEA region, this was attributed to strong demand from both the professional and DIY segments, with volume sales up significantly. Although pricing trends were positive in the region, the company’s price mix was impacted by strong growth in areas where average selling prices for paint are lower, viz. the Middle East and Africa.

In AkzoNobel’s Performance Coatings business, where its industrial coatings portfolio resides, the figures point to growth across the board. Here, the EMEA region is the largest contributor to sales in three of the four reporting segments, the exception being the Marine & Protective business, which is more naturally dominated by the strength of the Asian markets. The relative strengths of each region in terms of their contribution for 2020 are given in the bar chart. Hence the relative strengths of each region provide a background for understanding the following recoveries by segment as set out in the company’s interim report:

• Powder Coatings’ sales in the first half of 2021 rose by 29% and by 48% in second quarter alone. AkzoNobel enjoyed both demand and market share growth in this area, driven mainly by rising consumption from the automotive sector.

• Turnover in the Industrial Coatings operations grew by 16% in the first half and by 26% in the second quarter. There was growth in all sub-segments of the Industrial Coatings business in the second quarter, but particularly packaging coatings, which have performed consistently well during the pandemic conditions.

• In the Automotive & Specialty Coatings segment, vehicle refinishes continued to recover and aerospace coatings continued on their sequential quarterly path to recovery. The aerospace sector came good for AkzoNobel in terms of maintenance and repair. In the Automotive & Specialty Coatings segment, the second quarter registered a 39% increase in sales, which contributed to a 14% increase in sales in the first half of 2021 over 2020.

• Finally, the Marine & Protective operations that have a greater strength in the Asia Pacific region have seen the slowest return to growth, posting a 16% increase in sales in the second quarter, thereby contributing to 4% growth in the first half of the year. One of the strengths in this business was yacht coatings operations.

Tikkurila, which I profiled in the June 2021 issue of CW to highlight the scope of PPG’s acquisition, is also a key regional player based in Northern Europe, with special exposure to the markets of Scandinavia and the Baltic states. Russia and Sweden are its largest markets, taking 23% each, followed by Finland and Poland, which take a further 17% and 16% respectively.

Decorative paints constitute the vast majority of its business (84%), while industrial coatings operations covering the wood, protective and some OEM applications comprise the other 16%.

Revenues at Tikkurila rose by 7.4% in the second quarter of 2021, contributing to an increase of 8.3% for the first half of the year. Surprisingly, operating profits at the company were affected by costs – as measured across both periods – as a result of PPG’s tender offer.

Nevertheless, Tikkurila experienced good revenue growth in decorative paints in both the interior and exterior sub-segments. Revenue grew in all key geographies, except for Finland, where the second quarter revenue was slightly below the comparison period. Industrial paint revenues grew in both the metal and wood paints areas, when compared to the same time last year.

Among some of the key points for Tikkurila at the half-way stage in the year, the company’s interim CEO Markus Melkko said, “During the first half of the year, the global paint industry has experienced an unprecedented raw material disruption, which has further escalated during the second quarter. The raw material and packaging inflation impacted our cost basis, and the simultaneous raw material supply issues impacted our ability to serve our customers... Tikkurila experienced good revenue growth in decorative paints in both interior and exterior paints. Revenue grew in all key geographies, except in Finland, where the second quarter revenue was slightly below the comparison period. Industrial paint revenue grew in both metal and wood paints against the comparison period... We expect that raw material inflation and some supply constraints will continue during the second half of 2021. We will maintain focus on serving our customers to the best of our capabilities under the supply constraints, while maintaining our profitability with smart margin management and targeted pricing changes to offset inflation.”

Reports from Outside Europe

• PPG is AkzoNobel’s closest competitor in the EMEA region. Its architectural coatings activities are usually singled out for performance highlights when results are reported.

For the quarter ending with June 2021, PPG said that year-on-year net sales, excluding the impact of currency and acquisitions (organic sales), increased by a mid-teen percentage. The company reported sequential softening in the DIY paint segment, but this was more than offset by strong demand for architectural trade products.