Charles W. Thurston, Latin America Correspondent06.15.22

The outlook for growth in Latin America is positive, at close to 2% across the entire region, although the conjunction of factors affecting continued economic expansion has grown more complex of late.

Pre-COVID-19, questionable political will may have been the most unknown variable in predicting growth in Latin America. But today, apart from the ongoing pandemic, factors that have become critical to growth include inflation, commodity prices, supply chains and trade alliances, among others.

The implications of the evolving conditions in Latin America for US multinationals doing business in the region — including paint and coatings companies — may be profound, but ultimately rewarding, as the regional demand for goods and services rises.

In Brazil, the largest economy in the region, the outlook is confident, according to Luiz Cornacchioni, the executive president of the Associacao Brasileira dos Fabricantes de Tintas (Abrafati), the Brazilian Coatings Manufacturers Association. “There is a series of challenges and obstacles to be tackled by Brazil this year that have led to GDP growth forecasts of 0.5% to 1.0%.

However, expectations for the coatings industry are a little more optimistic: it should outgrow GDP by 1%, resulting in 1.5% to 2.0% growth,” Cornacchioni told CW in response to questions.

Normally, any positive average growth in regional GDP is considered good economic performance. However, many countries are still playing catch-up with GDP levels posted prior to COVID. “With the growth rates estimated for 2021 and 2022, less than half the countries in the region will have managed to recover the activity levels of 2019, before the crisis: 11 countries will achieve this in 2021 and a further three in 2022,” ECLAC says.

“This shows that the crisis caused by the pandemic has had lasting effects on economic growth in much of Latin America and the Caribbean and has aggravated the structural problems that already characterized the region before the crisis,” ECLAC opines.

Among the major Latin American economies, Argentina led GDP expansion, with 9.8%, followed by Colombia, with 9.5%; Mexico with 5.8%; and Brazil with 4.7% GDP expansion in 2021.

In Brazil, “We recognize that there are factors compromising (expected) better industry results that involve, on the one hand, disruption in international supply chains, which is aggravated by the war in Ukraine (reflecting in the shortage of certain raw materials and significant increases in their costs and in international freight prices), and, on the other hand, economic and political issues that are specific to Brazil: high inflation rates, interest rate hikes, and a sustained high rate of unemployment,” Cornacchioni said.

In Brazil’s Architectural segment, federal lending programs are helping boost demand. “Growth in 2022 sales of architectural paints will not be as significant as it was for the past two years (at around 5%), but this year we already are at a new, higher sales level,” said Cornacchioni.

“Other positive factors for sales of architectural paints and, in certain cases, other coatings, include the strength of agribusiness — which has ensured substantial growth in several regions in Brazil, the reopening of domestic travel — which has already begun, and boosting investments in renovations, improvements and new facilities,” Cornacchioni said.

Other factors involve in the recovery of Architectural segment sales include: “The fact that 2022 is an election year in Brazil, when there usually are many construction projects and economic stimulus measures in place, and the impact of the Auxílio Brasil federal income redistribution program, from which 18 million families are already benefiting, flooding the economy with a large amount of money,” Cornacchioni said.

In Brazil’s Industrial segment, “For industrial coatings, there are added positive prospects thanks to investments in infrastructure that have been boosted by new legislation on sanitation, and investments in various concessions recently granted in industries like transportation (including airports, highways and ports) and oil and gas. We can grow in 2022 at the same pace or even faster than we did in 2021, when our growth rate was 4%,” Cornacchioni said.

And in Brazil’s Automotive segment, “For OEM automotive coatings, we expect 2022 growth to be to the tune of 8%, in line with the forecasts for auto sales. There is pent-up demand due to a shortage of components experienced by the automotive industry in 2021,” said Cornacchioni.

Considering trade alone, Latin America is an accelerating engine of growth.

“From the perspective of the Latin American and Caribbean countries, the region’s exports are estimated to have grown by 25% in value in 2021, with export prices rising by 17% and volume by 8%,” ECLAC reports.

“Meanwhile, imports are estimated to have grown by 32% in value, the largest increase since 2010, when they rose by the same amount in the aftermath of the global financial crisis. After collapsing in 2020, the volume of imports is estimated to have risen by 20%, in line with the expansion of both domestic consumption and domestic investment in the region, with import prices also rising, by 12%,” according to the report.

New and stronger trade alliances, along with more regional integration, seem to be a key to achieving greater trade goals for countries in Latin America. Multiplying the number of trade pacts is one way that countries in the region can diversify and increase both exports and imports.

Argentina, for example, is considering joining the BRICS alliance, providing access the group’s new development bank. This development followed the Sino-Russian tour of President Alberto Fernández in early February. Other members of the trade group are Brazil, China, India, Russia and South Africa.

US-Latin American free trade is on the rise. “The United States has six free trade agreements (FTAs) with 12 countries: Mexico and Canada under the United States – Mexico–Canada Agreement (2020); Chile (2004); Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, and the Dominican Republic under the Dominican Republic–Central America–United States Free Trade Agreement (2006-2009); Peru (2009); Colombia (2012); and Panama (2012),” according to ECLAC.

“In addition, the United States has Trade and Investment Framework Agreements (TIFAs) or Trade and Investment Council Agreements (TICs) in force with Argentina, the Caribbean Community, Ecuador, Uruguay, and Paraguay. With Brazil, the United States has in force an Agreement on Trade and Economic Cooperation (ATEC) since 2011, updated in 2020 with a Protocol on Trade Rules and Transparency,” ECLAC relates.

The IADB has begun to cover the costs of companies moving operations from Asia and Europe to Latin America, especially in cases where the investment helps promote small and medium-sized businesses in the region.

Among target countries for such near-shoring investment are Colombia, Costa Rica, the Dominican Republic, Guatemala, Panama and Uruguay, according to think tank Wilson Center.

“Because of the increased perception of risk due to the pandemic, multinational corporations (MNC) have accelerated the reconfiguration of their Global Value Chains (GVCs). Many of these corporations are looking into geographically closer locations to source supplies, relocate or outsource their operations, or invest in existing assets. Such near-shoring is a central priority of the new IADB management and constitutes an opportunity for LAC SMEs (Latin America and the Caribbean Small and Medium Enterprises) that are capable of integration into these GVCs or becoming investment recipients,” IADB states in its new program, ConnectAmericas 2021: Facilitating Inclusive Trade and Near-shoring in LAC, launched in September 2021.

Near-shoring may also solve some of the problems with US-China trade, and with the new US focus on domestically-produced goods. “Reshoring is, and will continue to be, a vital element of the new, more resilient supply chains. It won’t be classic reshoring but an agile and dynamic rethinking of reshoring, incorporating and leveraging models where, for example, components and materials supplies are near-shored and final automated assembly and testing is done in the United States,” according to Kearny’s 2021 Reshoring Index.

“It’s an evolving definition that allows manufacturers to source a portion of their materials and components in nearby locations such as Mexico, Central America, and even Canada while still being able to say their products are manufactured in the United States,” Kearny suggests.

In Brazil, new investments have already begun, post-COVID. “We have seen a lot of investments made by manufacturers to launch products with focus on differentiation, which requires funds to be allocated to research and development, as well as marketing and promotional actions. This is currently a key investment driver. Several manufacturers are investing in facility and process upgrades and optimization, as well as capacity expansion, as a result of higher sales levels for the past two years,” said Cornacchioni.

Sub-regionally, however, the terms of trade fell by 5% in the Caribbean (excluding Guyana, Jamaica and Trinidad and Tobago) and by 1% in Central America, partly as a result of the large share of energy in the import baskets of these countries, ECLAC calculates.

“Conversely, it was precisely in the group of hydrocarbon-exporting countries (primarily Brazil, Venezuela, Mexico, Colombia, Argentina, Ecuador and Guyana) that the terms of trade rose the most – 15%,” the report points out.

US imports of oil from Latin America are rising rapidly now that Russian oil is blacklisted. “US refiners imported about 1.3 million barrels per day (bpd) of crude and fuel oil from Latin America in April, the highest in seven months according to US Customs data, as buyers began replacing Russian supplies,” Reuters reported on May 19. The trend has led the US government to revisit its relationship with Venezuela, long tied to Russia through loans.

Relief from inflation is not expected to take place before year’s end or early 2023, according to estimates by the Central Banks of the region, ECLAC notes. “A central element that will affect monetary policy dynamics in the region is the evolution of inflation, which has been on an upward trend since the second half of 2020. While inflation has been rising in all the countries, it is highest in those of South America, where it reached 7% in September 2021, up 3.9 percentage points from December 2020,” ECLAC says.

In Brazil, “Economic paints were the best sellers in 2020, reversing the upward trend for Premium paints. However, for 2021, Premium paints were the best sellers again. Each manufacturer has its own strategy in place for its product portfolio. From most there are Economic, Standard and Premium-grade paints available — as well as Super Premium paints, a new category officially launched in 2021 — to meet different requirements and markets. However, there are those who specialize in particular categories,” said Cornacchioni.

In Brazil, a long campaign by Abrafati to foster quality over price is meeting with substantial success. “This year marks the 20th anniversary of our industry-specific quality program for decorative paints. It is a success story, having raised overall quality levels in the market, fostered competition on an equal footing, and encouraged innovation. We continue to invent into improving and said Cornacchioni.

“We have been working to respond to changes in the business environment, market and technology, which have increasingly accelerated, involving reviews of important standards, new requirements, and additions of new products, colors and categories to the program. These are high-impact changes that are already driving the decorative paint market to an even higher quality level,” Cornacchioni concludes.

Pre-COVID-19, questionable political will may have been the most unknown variable in predicting growth in Latin America. But today, apart from the ongoing pandemic, factors that have become critical to growth include inflation, commodity prices, supply chains and trade alliances, among others.

The implications of the evolving conditions in Latin America for US multinationals doing business in the region — including paint and coatings companies — may be profound, but ultimately rewarding, as the regional demand for goods and services rises.

In Brazil, the largest economy in the region, the outlook is confident, according to Luiz Cornacchioni, the executive president of the Associacao Brasileira dos Fabricantes de Tintas (Abrafati), the Brazilian Coatings Manufacturers Association. “There is a series of challenges and obstacles to be tackled by Brazil this year that have led to GDP growth forecasts of 0.5% to 1.0%.

However, expectations for the coatings industry are a little more optimistic: it should outgrow GDP by 1%, resulting in 1.5% to 2.0% growth,” Cornacchioni told CW in response to questions.

GDP Growth To Drop in 2022

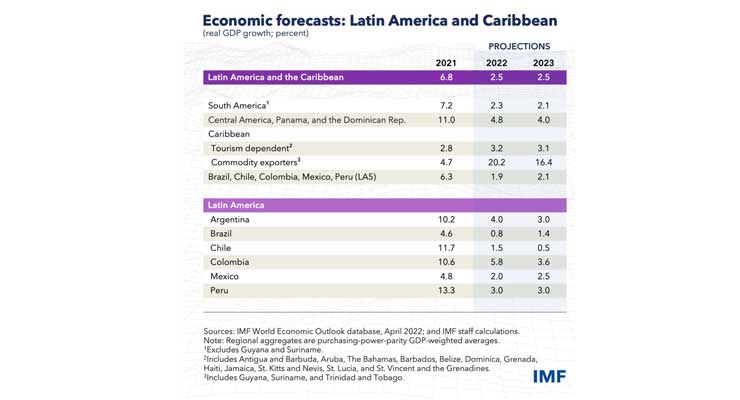

While regional growth was pegged at 6.2% during 2021, the outlook for gross domestic product expansion (GDP) is now only 1.8%, according to an April forecast revision by the United Nation’s Economic Commission for Latin America and the Caribbean (ECLAC). “In a context where the COVID-19 crisis exacerbated the region’s structural problems, adding further uncertainties and macroeconomic risks, the region’s economic growth is expected to slow (in) 2022,” ECLAC says in its Preliminary Overview of the Economies of Latin America and the Caribbean, released in January.Normally, any positive average growth in regional GDP is considered good economic performance. However, many countries are still playing catch-up with GDP levels posted prior to COVID. “With the growth rates estimated for 2021 and 2022, less than half the countries in the region will have managed to recover the activity levels of 2019, before the crisis: 11 countries will achieve this in 2021 and a further three in 2022,” ECLAC says.

“This shows that the crisis caused by the pandemic has had lasting effects on economic growth in much of Latin America and the Caribbean and has aggravated the structural problems that already characterized the region before the crisis,” ECLAC opines.

Top Country Growth Prospects

Among the countries with the strongest growth in 2021, Guyana was — and still is — the brightest light in the region, with GDP of 18.5% (See CW’s Latin America Report, May 2022). Other countries achieving double-digit increases in 2021 GDP included Peru, with 13.5%; Panama with 12.4%; Chile, with 11.8%; Dominican Republic, with 10.4%; and El Salvador, with 10%. These performances contrast with the regional average GDP increase of 6.3%, ECLAC research shows.Among the major Latin American economies, Argentina led GDP expansion, with 9.8%, followed by Colombia, with 9.5%; Mexico with 5.8%; and Brazil with 4.7% GDP expansion in 2021.

In Brazil, “We recognize that there are factors compromising (expected) better industry results that involve, on the one hand, disruption in international supply chains, which is aggravated by the war in Ukraine (reflecting in the shortage of certain raw materials and significant increases in their costs and in international freight prices), and, on the other hand, economic and political issues that are specific to Brazil: high inflation rates, interest rate hikes, and a sustained high rate of unemployment,” Cornacchioni said.

In Brazil’s Architectural segment, federal lending programs are helping boost demand. “Growth in 2022 sales of architectural paints will not be as significant as it was for the past two years (at around 5%), but this year we already are at a new, higher sales level,” said Cornacchioni.

“Other positive factors for sales of architectural paints and, in certain cases, other coatings, include the strength of agribusiness — which has ensured substantial growth in several regions in Brazil, the reopening of domestic travel — which has already begun, and boosting investments in renovations, improvements and new facilities,” Cornacchioni said.

Other factors involve in the recovery of Architectural segment sales include: “The fact that 2022 is an election year in Brazil, when there usually are many construction projects and economic stimulus measures in place, and the impact of the Auxílio Brasil federal income redistribution program, from which 18 million families are already benefiting, flooding the economy with a large amount of money,” Cornacchioni said.

In Brazil’s Industrial segment, “For industrial coatings, there are added positive prospects thanks to investments in infrastructure that have been boosted by new legislation on sanitation, and investments in various concessions recently granted in industries like transportation (including airports, highways and ports) and oil and gas. We can grow in 2022 at the same pace or even faster than we did in 2021, when our growth rate was 4%,” Cornacchioni said.

And in Brazil’s Automotive segment, “For OEM automotive coatings, we expect 2022 growth to be to the tune of 8%, in line with the forecasts for auto sales. There is pent-up demand due to a shortage of components experienced by the automotive industry in 2021,” said Cornacchioni.

Trade Alliances More Attractive

Many of the issues affecting regional growth will be the focus of international working groups at the Summit of the Americas, scheduled in Los Angeles in early June, the first US hosting of the event in nearly 30 years. The value of US-Latin America trade is massive, particularly in the case of US exports. The top five US export markets to the Western Hemisphere in 2019 (latest year cited) were: Canada at $292.6 billion, Mexico at $256.6 billion, Brazil at $42.9 billion, Chile at $15.7 billion, and Colombia at $14.7 billion, according to the US Trade Representative.Considering trade alone, Latin America is an accelerating engine of growth.

“From the perspective of the Latin American and Caribbean countries, the region’s exports are estimated to have grown by 25% in value in 2021, with export prices rising by 17% and volume by 8%,” ECLAC reports.

“Meanwhile, imports are estimated to have grown by 32% in value, the largest increase since 2010, when they rose by the same amount in the aftermath of the global financial crisis. After collapsing in 2020, the volume of imports is estimated to have risen by 20%, in line with the expansion of both domestic consumption and domestic investment in the region, with import prices also rising, by 12%,” according to the report.

New and stronger trade alliances, along with more regional integration, seem to be a key to achieving greater trade goals for countries in Latin America. Multiplying the number of trade pacts is one way that countries in the region can diversify and increase both exports and imports.

Argentina, for example, is considering joining the BRICS alliance, providing access the group’s new development bank. This development followed the Sino-Russian tour of President Alberto Fernández in early February. Other members of the trade group are Brazil, China, India, Russia and South Africa.

US-Latin American free trade is on the rise. “The United States has six free trade agreements (FTAs) with 12 countries: Mexico and Canada under the United States – Mexico–Canada Agreement (2020); Chile (2004); Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, and the Dominican Republic under the Dominican Republic–Central America–United States Free Trade Agreement (2006-2009); Peru (2009); Colombia (2012); and Panama (2012),” according to ECLAC.

“In addition, the United States has Trade and Investment Framework Agreements (TIFAs) or Trade and Investment Council Agreements (TICs) in force with Argentina, the Caribbean Community, Ecuador, Uruguay, and Paraguay. With Brazil, the United States has in force an Agreement on Trade and Economic Cooperation (ATEC) since 2011, updated in 2020 with a Protocol on Trade Rules and Transparency,” ECLAC relates.

Near-Shoring to Boost LatAm Production

As global supply chain woes continue to slow trade and increase costs, the concept of near-shoring, or moving investments into supply links closer to the United States, is evolving rapidly. For example, Inter-American Development Bank (IADB) president Mauricio Claver-Carone’s Vision 2025 plan for economic recovery and growth in the Americas is focused on near-shoring.The IADB has begun to cover the costs of companies moving operations from Asia and Europe to Latin America, especially in cases where the investment helps promote small and medium-sized businesses in the region.

Among target countries for such near-shoring investment are Colombia, Costa Rica, the Dominican Republic, Guatemala, Panama and Uruguay, according to think tank Wilson Center.

“Because of the increased perception of risk due to the pandemic, multinational corporations (MNC) have accelerated the reconfiguration of their Global Value Chains (GVCs). Many of these corporations are looking into geographically closer locations to source supplies, relocate or outsource their operations, or invest in existing assets. Such near-shoring is a central priority of the new IADB management and constitutes an opportunity for LAC SMEs (Latin America and the Caribbean Small and Medium Enterprises) that are capable of integration into these GVCs or becoming investment recipients,” IADB states in its new program, ConnectAmericas 2021: Facilitating Inclusive Trade and Near-shoring in LAC, launched in September 2021.

Near-shoring may also solve some of the problems with US-China trade, and with the new US focus on domestically-produced goods. “Reshoring is, and will continue to be, a vital element of the new, more resilient supply chains. It won’t be classic reshoring but an agile and dynamic rethinking of reshoring, incorporating and leveraging models where, for example, components and materials supplies are near-shored and final automated assembly and testing is done in the United States,” according to Kearny’s 2021 Reshoring Index.

“It’s an evolving definition that allows manufacturers to source a portion of their materials and components in nearby locations such as Mexico, Central America, and even Canada while still being able to say their products are manufactured in the United States,” Kearny suggests.

In Brazil, new investments have already begun, post-COVID. “We have seen a lot of investments made by manufacturers to launch products with focus on differentiation, which requires funds to be allocated to research and development, as well as marketing and promotional actions. This is currently a key investment driver. Several manufacturers are investing in facility and process upgrades and optimization, as well as capacity expansion, as a result of higher sales levels for the past two years,” said Cornacchioni.

Oil Trade Morphs To Favor Latin America

Across the region, the “terms of trade” produced a 5% rise during 2021, ECLAC reckons. The terms of trade is the relative price of exports in terms of imports and is defined as the ratio of export prices to import prices. It can be interpreted as the amount of import goods an economy can purchase per unit of export goods, says Wikipedia.Sub-regionally, however, the terms of trade fell by 5% in the Caribbean (excluding Guyana, Jamaica and Trinidad and Tobago) and by 1% in Central America, partly as a result of the large share of energy in the import baskets of these countries, ECLAC calculates.

“Conversely, it was precisely in the group of hydrocarbon-exporting countries (primarily Brazil, Venezuela, Mexico, Colombia, Argentina, Ecuador and Guyana) that the terms of trade rose the most – 15%,” the report points out.

US imports of oil from Latin America are rising rapidly now that Russian oil is blacklisted. “US refiners imported about 1.3 million barrels per day (bpd) of crude and fuel oil from Latin America in April, the highest in seven months according to US Customs data, as buyers began replacing Russian supplies,” Reuters reported on May 19. The trend has led the US government to revisit its relationship with Venezuela, long tied to Russia through loans.

Limits to Growth: Rising Inflation

One major contributing factor to slower growth is inflation. “In 2021, inflationary pressures were observed in the majority of the region’s countries, led by price increases in food and energy (inflation reached 7.1% on average by November, excluding Argentina, Haiti, Surinam and Venezuela), and these pressures are expected to continue in 2022,” ECLAC reported.Relief from inflation is not expected to take place before year’s end or early 2023, according to estimates by the Central Banks of the region, ECLAC notes. “A central element that will affect monetary policy dynamics in the region is the evolution of inflation, which has been on an upward trend since the second half of 2020. While inflation has been rising in all the countries, it is highest in those of South America, where it reached 7% in September 2021, up 3.9 percentage points from December 2020,” ECLAC says.

In Brazil, “Economic paints were the best sellers in 2020, reversing the upward trend for Premium paints. However, for 2021, Premium paints were the best sellers again. Each manufacturer has its own strategy in place for its product portfolio. From most there are Economic, Standard and Premium-grade paints available — as well as Super Premium paints, a new category officially launched in 2021 — to meet different requirements and markets. However, there are those who specialize in particular categories,” said Cornacchioni.

Quality Gaining Ground Over Low Price

While manufacturing in China has tapped into some of the lowest labor prices in the world, disruptions — and higher prices — in the global supply chain have encouraged companies to reconsider quality over cost.In Brazil, a long campaign by Abrafati to foster quality over price is meeting with substantial success. “This year marks the 20th anniversary of our industry-specific quality program for decorative paints. It is a success story, having raised overall quality levels in the market, fostered competition on an equal footing, and encouraged innovation. We continue to invent into improving and said Cornacchioni.

“We have been working to respond to changes in the business environment, market and technology, which have increasingly accelerated, involving reviews of important standards, new requirements, and additions of new products, colors and categories to the program. These are high-impact changes that are already driving the decorative paint market to an even higher quality level,” Cornacchioni concludes.