Gary Shawhan, The CHEMARK Consulting Group09.22.23

Business goals are a management tool employed to guide or direct different levels of the organization to improve, achieve, or focus on issues important to the future health and growth of the company. Meaningful goals are ones that have a well-defined purpose, have been clearly communicated to all the key stakeholders, and are backed by supporting details sufficient to gain buy-in.

Regardless of the business situation, when setting goals two key questions need to be answered that determine how important and actionable these goals really are. First, who is setting the goals? Second, how are the individuals who are setting the goals holding those involved in the execution accountable for their effort and the results?

What determines who sets the goals? The scope of the business issues being addressed (in goal setting) is a key determinant of who in the organization should lead the effort of setting the goals. In addition, the individual organizational structure of the company and the management team also has a significant influence on where (in the company) goals are set and who is responsible for managing accountability for the results.

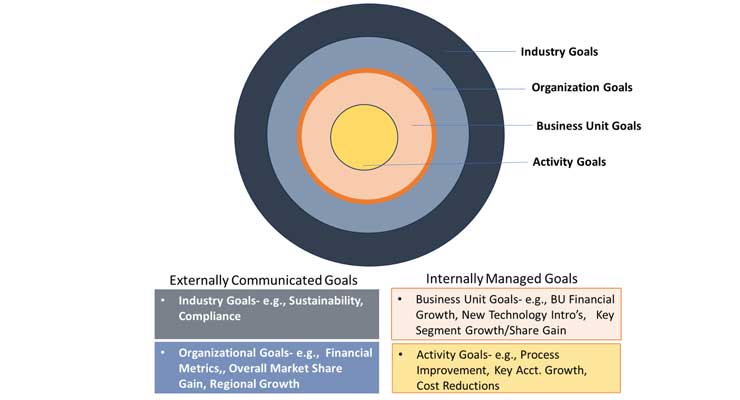

Figure 1 suggests a “hierarchy of scope” that identifies four (4) different categories of business circumstances where goal setting is employed as a business tool. As identified in Figure 1, certain goals are set by the company that reflect the current expectations and direction of the business. Other goals reveal the longer-term vison and business objectives for the company. These goals are normally intended to be communicated externally to the industry at large.

Certain goals are intended to address more specific areas for improvement or growth within individual business units or as they relate to the performance of individuals or departments. These goals are normally held internally to the company and not intended to be communicated externally to industry.

In global companies, organizational goals may or may not be tailored to accommodate regional differences in the business climate and market conditions. When senior management works collaboratively with management from key strategic regions to adjust certain goals to reflect differences in the business situation, it normally produces more meaningful results.

When management practice permits a high level of regional discretion and autonomy, meaningful goal setting for the company at either the industry or organization level can be very difficult to achieve. Most important, senior management can wind up having difficulty in communicating a singular business direction to industry.

In contrast, there are situations where the senior management team dictates one set of goals across the entire organization irrespective of regional differences. This approach has the advantage of providing clarity to all those in the company and to industry as well on what management expects.

At the same time, by not incorporating some adjustments to the company’s business goals to accommodate regional differences, it can be confusing if not discouraging to business unit managers and their employees in certain regions. They see that the company goals do not have a reasonable fit with “their” markets and the needs of their customers.

This disconnect (for certain regions) with a singular set of business goals is amplified when competing for internal resources out of a single company pot or fund. This approach can also send unintended messages to the industry about the direction of the company and its commitment to certain geographic regions.

Industry goals must originate from top-level management, normally the President, CEO, or Managing Director. Within the company, they need to be communicated across all elements of the organization. Externally, there needs to be a well-planned and executed communication plan that reaches out to the financial sector, the various elements of the value-chain, the customer base, and even competitors.

For industry goals, Individual accountabilities is more difficult to assign below the level of senior management. Senior management has the primary responsibility to initiate actions and direct others to participate and support these goals as an overriding objective for the company.

Setting organization-level goals is a fundamental aspect of successful business management. Financial analysis and tracking of financial and business data against historical numbers is the responsibility of senior management.

Establishing and communicating both the financial and the business goals for the organization is a critical part of doing business. Investors, stockholders, and the investment community expect to have access to this information on a regular basis to support their investment decisions.

Organization-level goals are set by the senior management team. The format within which these goals are set, however, is very individual to each company and its organizational structure. Emphasis and prioritizing goals are dependent on the actual business situation the company currently faces in the marketplace.

Accountability for meeting organizational goals normally extends down to the management teams at each operating group, division, or entity for which these overriding organizational goals are set.

Setting business unit, divisional, or business group goals are normally ones that are held internally rather than communicated to industry. These goals are used by the individual management teams in several different ways.

First, goal setting creates focus and reinforces priorities for the business unit going forward. Second, they provide managers, within the business unit, a basis for setting their own performance improvement targets. This, in turn, can be used to establish individual incentive compensation plans. In addition, some of these goals are often intended to dovetail with the goals established for the organization as a whole.

Accountability for results, based on goals set at the business unit level, is dependent on the way the organization is structured. It is also based on how senior management is able to integrate goal setting into the strategic planning process. When there is significant alignment of business objectives and the goals for achieving them across the management chain, the ability to hold managers and their subordinates accountable for results is significantly greater.

Activity-related goals apply to a wide range of business elements- both internal and external to the organization. These goals are normally directed at departments or individuals within the organization and expressed as targets for improvement or change over what is current practice.

For internally directed goals the focus is often on specific issues where change is needed to improve the health of the business going forward. Examples of internally directed goals include quality control, process improvement, purchasing practices, etc..

External activity-related goals are linked to the marketplace and include customers and efforts to address issues that will improve the overall economic health of the company. Examples include sales territory revenue growth, channel-to-market position improvement, or new product introductions targeting key trends or unmet needs in the marketplace.

Accountability for improvement in activity-related issues is not always a well-defined and monitored process. The individual importance of each item for which goals are set and the level of attention given to it by unit managers or supervisors varies widely.

Regardless of the business situation, when setting goals two key questions need to be answered that determine how important and actionable these goals really are. First, who is setting the goals? Second, how are the individuals who are setting the goals holding those involved in the execution accountable for their effort and the results?

What determines who sets the goals? The scope of the business issues being addressed (in goal setting) is a key determinant of who in the organization should lead the effort of setting the goals. In addition, the individual organizational structure of the company and the management team also has a significant influence on where (in the company) goals are set and who is responsible for managing accountability for the results.

Figure 1 suggests a “hierarchy of scope” that identifies four (4) different categories of business circumstances where goal setting is employed as a business tool. As identified in Figure 1, certain goals are set by the company that reflect the current expectations and direction of the business. Other goals reveal the longer-term vison and business objectives for the company. These goals are normally intended to be communicated externally to the industry at large.

Certain goals are intended to address more specific areas for improvement or growth within individual business units or as they relate to the performance of individuals or departments. These goals are normally held internally to the company and not intended to be communicated externally to industry.

In global companies, organizational goals may or may not be tailored to accommodate regional differences in the business climate and market conditions. When senior management works collaboratively with management from key strategic regions to adjust certain goals to reflect differences in the business situation, it normally produces more meaningful results.

When management practice permits a high level of regional discretion and autonomy, meaningful goal setting for the company at either the industry or organization level can be very difficult to achieve. Most important, senior management can wind up having difficulty in communicating a singular business direction to industry.

In contrast, there are situations where the senior management team dictates one set of goals across the entire organization irrespective of regional differences. This approach has the advantage of providing clarity to all those in the company and to industry as well on what management expects.

At the same time, by not incorporating some adjustments to the company’s business goals to accommodate regional differences, it can be confusing if not discouraging to business unit managers and their employees in certain regions. They see that the company goals do not have a reasonable fit with “their” markets and the needs of their customers.

This disconnect (for certain regions) with a singular set of business goals is amplified when competing for internal resources out of a single company pot or fund. This approach can also send unintended messages to the industry about the direction of the company and its commitment to certain geographic regions.

Communicating Differences in Goal Setting based on Business Scope

Industry goals are linked to “big picture” issues. Today, an excellent example of this is sustainability. Major industry players, including market leaders and important market challengers, are engaged in a pro-active effort to strengthen the company image and show their long-term commitment to sustainability.Industry goals must originate from top-level management, normally the President, CEO, or Managing Director. Within the company, they need to be communicated across all elements of the organization. Externally, there needs to be a well-planned and executed communication plan that reaches out to the financial sector, the various elements of the value-chain, the customer base, and even competitors.

For industry goals, Individual accountabilities is more difficult to assign below the level of senior management. Senior management has the primary responsibility to initiate actions and direct others to participate and support these goals as an overriding objective for the company.

Setting organization-level goals is a fundamental aspect of successful business management. Financial analysis and tracking of financial and business data against historical numbers is the responsibility of senior management.

Establishing and communicating both the financial and the business goals for the organization is a critical part of doing business. Investors, stockholders, and the investment community expect to have access to this information on a regular basis to support their investment decisions.

Organization-level goals are set by the senior management team. The format within which these goals are set, however, is very individual to each company and its organizational structure. Emphasis and prioritizing goals are dependent on the actual business situation the company currently faces in the marketplace.

Accountability for meeting organizational goals normally extends down to the management teams at each operating group, division, or entity for which these overriding organizational goals are set.

Setting business unit, divisional, or business group goals are normally ones that are held internally rather than communicated to industry. These goals are used by the individual management teams in several different ways.

First, goal setting creates focus and reinforces priorities for the business unit going forward. Second, they provide managers, within the business unit, a basis for setting their own performance improvement targets. This, in turn, can be used to establish individual incentive compensation plans. In addition, some of these goals are often intended to dovetail with the goals established for the organization as a whole.

Accountability for results, based on goals set at the business unit level, is dependent on the way the organization is structured. It is also based on how senior management is able to integrate goal setting into the strategic planning process. When there is significant alignment of business objectives and the goals for achieving them across the management chain, the ability to hold managers and their subordinates accountable for results is significantly greater.

Activity-related goals apply to a wide range of business elements- both internal and external to the organization. These goals are normally directed at departments or individuals within the organization and expressed as targets for improvement or change over what is current practice.

For internally directed goals the focus is often on specific issues where change is needed to improve the health of the business going forward. Examples of internally directed goals include quality control, process improvement, purchasing practices, etc..

External activity-related goals are linked to the marketplace and include customers and efforts to address issues that will improve the overall economic health of the company. Examples include sales territory revenue growth, channel-to-market position improvement, or new product introductions targeting key trends or unmet needs in the marketplace.

Accountability for improvement in activity-related issues is not always a well-defined and monitored process. The individual importance of each item for which goals are set and the level of attention given to it by unit managers or supervisors varies widely.