01.26.18

PPG Industries (PPG: Buy, $127 PT)

Volume Acceleration Drives Penny Beat, Despite Margin Pressure

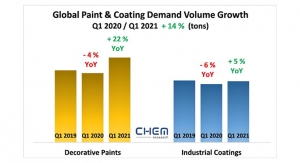

• 4Q EPS brings best volume growth in 3 years, although margin challenge continues. We are encouraged by strength in sales, supported by better volume growth, yet cost inflation continues to pressure margins. On balance, PPG posted adjusted 4Q17 EPS of $1.19A, a penny ahead of consensus of $1.18 and a penny shy of our $1.20E. As expected, natural disaster-related costs posed a headwind of $0.05 in 4Q. Sales of $3.68bn reflect markedly improved volume growth of 3%, supplemented by more than +3% from FX and modest contributions from price. Volume growth of +3% y-y in 4Q17 was the best result since 4Q14 and represented a meaningful acceleration +0.9% in 2015, +1.0% in 2016 and +0.8% during the first nine months of 2017 (or ~ 1% ex natural disasters). Price did improve on a sequential basis for the third consecutive quarter, albeit not enough to offset raw material cost pressures with global epoxy prices the latest to percolate higher in 4Q. As a result, combined EBIT margin for PPG’s two coatings segments eroded 110bps y-y.

• Pace of capital deployment accelerated. PPG deployed $400mn for repurchases on the quarter, accelerating from $250mn in 3Q17. Management committed to capital deployment of $2.4bn in 2018, or 8.1% of the company’s equity market capitalization. This pace is now consistent with our thesis that PPG can deploy $200mn per month for the next 3 years or more.

• Performance Coatings earnings came in light despite sales upside. Sales of $2.1bn came in ahead of both our $2.05bn and the Street at $2.07bn. Volume growth of over 2% y-y, despite the ongoing hurricane and earthquake related impacts, is encouraging, as is the commentary around price traction, which was said to be higher across most businesses and regions. However, segment EBIT of $260mn was a net EPS headwind of $0.03 against the $269mn that we had forecast as margins came in 90bps lower than expected. Volumes in EMEA were flat y-y, a nice reversal from the mid-single digit volume decline in 3Q17 as business had been turned away due to either lower profitability or lack of consumer acceptance of higher prices. A continued rebound in European volumes would read positively for profitability given the strong incremental margins that PPG tends to realize in that market. The US DIY paint market was said to be flat y-y across big box and independent retailers, which we read as “glass half full” for the big box channel given chronic volume erosion among the independents. Meanwhile, PPG’s company-owned stores continue to gain traction, with solid mid-single digit growth. Volumes at the protective and marine business continue to bottom out with the second consecutive quarter of flat y-y performance. Finally, organic sales growth in both aerospace and auto refinish coatings trended up mid-single digits as both businesses continue their consistent performance.

• Industrial Coatings margins also disappoint. EBIT of $212mn came in just below our $215mn and well below the Street’s $233mn. Sales trended ahead of our forecast, leaving a 90bp margin miss to drive the EPS variance of -$0.01. Unfortunately, year over year margin degradation of 280bps is actually a slight acceleration from the -230bs reported in 3Q17 and -270bps in 2Q17. Pricing continues to be a net headwind y-y, though the company did indicate a better capture sequentially from 3Q. Encouragingly, volumes in the segment grew more than 4%, an improvement from +3% in 3Q17, and FX represented an additional 3% tailwind. General industrial volumes continue to flourish, up mid-single digits, as it appears that positive economic momentum is following through to PPG sales. Packaging coatings led the segment, up high-single digits from the mid-single digit growth of 3Q, which we attribute to the adoption of new technologies (BPA-NI). Finally, auto OEM volumes grew low-single digits, generally in line with global industry production rates.

• We rate PPG shares Buy with a price target of $127. Our target suggests total upside potential of 12%, including a dividend yield of 1.6%. PPG trades at a multiple of 2018 EBITDA of 11.7x, which is the lowest among four coatings stocks in our coverage and 1.3x below the average of 13.0x for the coatings cohort. On a P/E basis, PPG now trades at a 2018 multiple of 17.7x, which represents a discount of 3.7x or 17% vs. the average of three US coatings peers (SHW, AXTA and RPM). Our valuation of PPG is based on an average of two methodologies: DCF analysis and a relative P/E framework. Our DCF analysis suggests a warranted stock price of $125. Using our relative P/E framework wherein we apply a 5% premium to the S&P500 multiple, we calculate warranted value of $129 per PPG share.

(Please see full report for details)

Volume Acceleration Drives Penny Beat, Despite Margin Pressure

• 4Q EPS brings best volume growth in 3 years, although margin challenge continues. We are encouraged by strength in sales, supported by better volume growth, yet cost inflation continues to pressure margins. On balance, PPG posted adjusted 4Q17 EPS of $1.19A, a penny ahead of consensus of $1.18 and a penny shy of our $1.20E. As expected, natural disaster-related costs posed a headwind of $0.05 in 4Q. Sales of $3.68bn reflect markedly improved volume growth of 3%, supplemented by more than +3% from FX and modest contributions from price. Volume growth of +3% y-y in 4Q17 was the best result since 4Q14 and represented a meaningful acceleration +0.9% in 2015, +1.0% in 2016 and +0.8% during the first nine months of 2017 (or ~ 1% ex natural disasters). Price did improve on a sequential basis for the third consecutive quarter, albeit not enough to offset raw material cost pressures with global epoxy prices the latest to percolate higher in 4Q. As a result, combined EBIT margin for PPG’s two coatings segments eroded 110bps y-y.

• Pace of capital deployment accelerated. PPG deployed $400mn for repurchases on the quarter, accelerating from $250mn in 3Q17. Management committed to capital deployment of $2.4bn in 2018, or 8.1% of the company’s equity market capitalization. This pace is now consistent with our thesis that PPG can deploy $200mn per month for the next 3 years or more.

• Performance Coatings earnings came in light despite sales upside. Sales of $2.1bn came in ahead of both our $2.05bn and the Street at $2.07bn. Volume growth of over 2% y-y, despite the ongoing hurricane and earthquake related impacts, is encouraging, as is the commentary around price traction, which was said to be higher across most businesses and regions. However, segment EBIT of $260mn was a net EPS headwind of $0.03 against the $269mn that we had forecast as margins came in 90bps lower than expected. Volumes in EMEA were flat y-y, a nice reversal from the mid-single digit volume decline in 3Q17 as business had been turned away due to either lower profitability or lack of consumer acceptance of higher prices. A continued rebound in European volumes would read positively for profitability given the strong incremental margins that PPG tends to realize in that market. The US DIY paint market was said to be flat y-y across big box and independent retailers, which we read as “glass half full” for the big box channel given chronic volume erosion among the independents. Meanwhile, PPG’s company-owned stores continue to gain traction, with solid mid-single digit growth. Volumes at the protective and marine business continue to bottom out with the second consecutive quarter of flat y-y performance. Finally, organic sales growth in both aerospace and auto refinish coatings trended up mid-single digits as both businesses continue their consistent performance.

• Industrial Coatings margins also disappoint. EBIT of $212mn came in just below our $215mn and well below the Street’s $233mn. Sales trended ahead of our forecast, leaving a 90bp margin miss to drive the EPS variance of -$0.01. Unfortunately, year over year margin degradation of 280bps is actually a slight acceleration from the -230bs reported in 3Q17 and -270bps in 2Q17. Pricing continues to be a net headwind y-y, though the company did indicate a better capture sequentially from 3Q. Encouragingly, volumes in the segment grew more than 4%, an improvement from +3% in 3Q17, and FX represented an additional 3% tailwind. General industrial volumes continue to flourish, up mid-single digits, as it appears that positive economic momentum is following through to PPG sales. Packaging coatings led the segment, up high-single digits from the mid-single digit growth of 3Q, which we attribute to the adoption of new technologies (BPA-NI). Finally, auto OEM volumes grew low-single digits, generally in line with global industry production rates.

• We rate PPG shares Buy with a price target of $127. Our target suggests total upside potential of 12%, including a dividend yield of 1.6%. PPG trades at a multiple of 2018 EBITDA of 11.7x, which is the lowest among four coatings stocks in our coverage and 1.3x below the average of 13.0x for the coatings cohort. On a P/E basis, PPG now trades at a 2018 multiple of 17.7x, which represents a discount of 3.7x or 17% vs. the average of three US coatings peers (SHW, AXTA and RPM). Our valuation of PPG is based on an average of two methodologies: DCF analysis and a relative P/E framework. Our DCF analysis suggests a warranted stock price of $125. Using our relative P/E framework wherein we apply a 5% premium to the S&P500 multiple, we calculate warranted value of $129 per PPG share.

(Please see full report for details)