09.18.17

DowDuPont Incorporated (DWDP: Buy, $74 PT)

Shape Shifting; Affirm Buy on Portfolio Recast

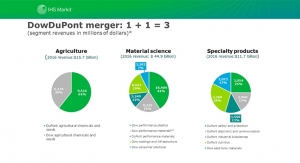

• We view this morning’s portfolio update favorably. We’d highlight several key takeaways from DowDuPont’s update and impromptu conference call at 8:30AM ET today: (1) the magnitude of the portfolio shift of $8bn in sales and $2.4bn of EBITDA is quite similar to that outlined in our recent deep dive (click here and see Figure 5), albeit with a somewhat different mix; (2) while constructive for shareholder value as we discuss below, the shift will bring some dis-synergies, but these are apparently not meaningful enough to alter the company’s overall targets, which were affirmed; (3) Hurricane Harvey-related impact of $250mn in 3Q17 is unsurprising and temporary in nature, but will contribute to the “messy” nature of 3Q17 as a transition quarter; and (4) other financial disclosures appear in line with a few expectations: (A) D&A looks $425mn higher than we had modeled for 2018, or $0.13 in EPS terms due to a higher step-up; and (B) the new tax rate range of 25-29% is likewise higher than our 24.5%, which would translate to $0.14 in EPS terms at the midpoint. Neither of these issues will compromise EBITDA, so the tension in our sum-of-the-parts (SOTP) valuation framework is upward, not downward.

• DowDuPont’s new portfolio mix strikes us as sensible and defensible. We believe the shift can create/unlock value of $7-8bn as compared to the portfolio composition as intended previously. This represents ~5% of the company’s equity market capitalization, although we believe a portion of this figure is already embedded in the DWDP stock price. At a high level, DowDuPont is shifting more than $8bn in sales and $2.4bn in operating EBITDA from the Materials Science Division to the Specialty Products Division. This is essentially in line with the $8.13bn in revenue and $2.25bn in EBITDA that we had hypothesized would be open for realignment in our report last week. However, the company...

• Hurricane Harvey making its presence felt, but we suggest you look past. DowDuPont is guiding to a pro forma negative $250mn EBITDA headwind from the impacts of Hurricane Harvey on the Texas Gulf Coast. We assume this headwind is from a combination of extended outages at legacy Dow and DuPont ethylene and polyethylene (PE) resin facilities as well as lower overall sales volumes into the local market. We caution investors from penalizing shares based on this however for three reasons. The first is...

• Pro forma modeling guidance paints a mixed picture. Pro forma 3Q17 D&A guidance of $1.35-1.45bn implies an annual range of $5.4-5.8bn, which is about $425mn higher than our estimate of almost $5.2bn. Implied annual net interest expense of $1.2-1.4bn is more in line with the $1.2bn that we had penciled in. There is also an additional $100mn in headwinds to EBITDA given the reallocation of DuPont’s legacy pension and hedging losses into the segment results, although we note that only $50mn of this $100mn is a new item and thus will carry an EPS impact. The other $50mn represents a shift in line item and thus has a neutral EPS impact. Additionally...

• DWDP remains our top pick with a price target of $74. Our target suggests total upside potential of 13%, inclusive of the dividend which is yet to be determined by the company’s new board of directors (Dow’s old dividend was $1.84 per annum, which would imply a yield of 2.8%). Given a pending break-up into three separate companies, we continue to assess the value of DWDP shares using a sum-of-the parts (SOTP) framework for the combined entity, DowDuPont, including synergies and underfunded pension liabilities. DWDP now trades at a 2018 P/E multiple of 16.3x, which represents a discount of 6% vs. the average of our 16 chemical companies under coverage. Likewise, DWDP trades for 9.4x our 2018 EBITDA vs. an average of 10.3x for the sector. We believe these multiples are too low for a catalyst-rich stock with a forward looking 3-year EPS CAGR of 11%+, or a premium of 400bps vs. the average for the US chemicals sector. Following are our published SOTP analyses and financial model, as unadjusted for today’s developments.

(Please see full report for details)

Shape Shifting; Affirm Buy on Portfolio Recast

• We view this morning’s portfolio update favorably. We’d highlight several key takeaways from DowDuPont’s update and impromptu conference call at 8:30AM ET today: (1) the magnitude of the portfolio shift of $8bn in sales and $2.4bn of EBITDA is quite similar to that outlined in our recent deep dive (click here and see Figure 5), albeit with a somewhat different mix; (2) while constructive for shareholder value as we discuss below, the shift will bring some dis-synergies, but these are apparently not meaningful enough to alter the company’s overall targets, which were affirmed; (3) Hurricane Harvey-related impact of $250mn in 3Q17 is unsurprising and temporary in nature, but will contribute to the “messy” nature of 3Q17 as a transition quarter; and (4) other financial disclosures appear in line with a few expectations: (A) D&A looks $425mn higher than we had modeled for 2018, or $0.13 in EPS terms due to a higher step-up; and (B) the new tax rate range of 25-29% is likewise higher than our 24.5%, which would translate to $0.14 in EPS terms at the midpoint. Neither of these issues will compromise EBITDA, so the tension in our sum-of-the-parts (SOTP) valuation framework is upward, not downward.

• DowDuPont’s new portfolio mix strikes us as sensible and defensible. We believe the shift can create/unlock value of $7-8bn as compared to the portfolio composition as intended previously. This represents ~5% of the company’s equity market capitalization, although we believe a portion of this figure is already embedded in the DWDP stock price. At a high level, DowDuPont is shifting more than $8bn in sales and $2.4bn in operating EBITDA from the Materials Science Division to the Specialty Products Division. This is essentially in line with the $8.13bn in revenue and $2.25bn in EBITDA that we had hypothesized would be open for realignment in our report last week. However, the company...

• Hurricane Harvey making its presence felt, but we suggest you look past. DowDuPont is guiding to a pro forma negative $250mn EBITDA headwind from the impacts of Hurricane Harvey on the Texas Gulf Coast. We assume this headwind is from a combination of extended outages at legacy Dow and DuPont ethylene and polyethylene (PE) resin facilities as well as lower overall sales volumes into the local market. We caution investors from penalizing shares based on this however for three reasons. The first is...

• Pro forma modeling guidance paints a mixed picture. Pro forma 3Q17 D&A guidance of $1.35-1.45bn implies an annual range of $5.4-5.8bn, which is about $425mn higher than our estimate of almost $5.2bn. Implied annual net interest expense of $1.2-1.4bn is more in line with the $1.2bn that we had penciled in. There is also an additional $100mn in headwinds to EBITDA given the reallocation of DuPont’s legacy pension and hedging losses into the segment results, although we note that only $50mn of this $100mn is a new item and thus will carry an EPS impact. The other $50mn represents a shift in line item and thus has a neutral EPS impact. Additionally...

• DWDP remains our top pick with a price target of $74. Our target suggests total upside potential of 13%, inclusive of the dividend which is yet to be determined by the company’s new board of directors (Dow’s old dividend was $1.84 per annum, which would imply a yield of 2.8%). Given a pending break-up into three separate companies, we continue to assess the value of DWDP shares using a sum-of-the parts (SOTP) framework for the combined entity, DowDuPont, including synergies and underfunded pension liabilities. DWDP now trades at a 2018 P/E multiple of 16.3x, which represents a discount of 6% vs. the average of our 16 chemical companies under coverage. Likewise, DWDP trades for 9.4x our 2018 EBITDA vs. an average of 10.3x for the sector. We believe these multiples are too low for a catalyst-rich stock with a forward looking 3-year EPS CAGR of 11%+, or a premium of 400bps vs. the average for the US chemicals sector. Following are our published SOTP analyses and financial model, as unadjusted for today’s developments.

(Please see full report for details)